Turkey sees benign inflation in March, but upside risks for April

Turkey's March data shows a better-than-expected turnout, but recent currency weakness could result in upward pressure on April inflation

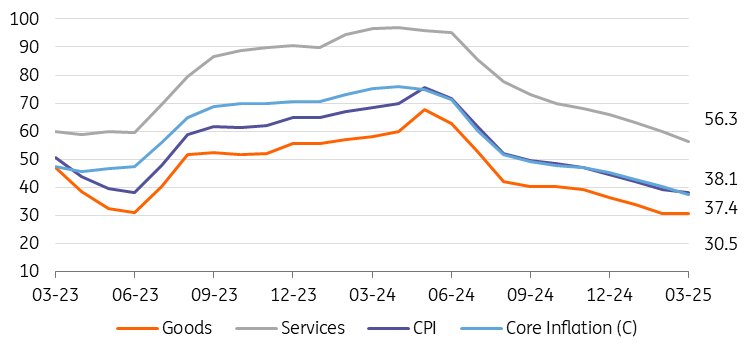

Turkish inflation stood at 2.46% month-on-month in March, coming in below the consensus of 2.9%. As a result, annual inflation continued to decline, dropping to 38.1% year-on-year, down from 39.1% in February. However, it remained above the Central Bank of Turkey's (CBT) forecast of 24% (with a forecast range of 19-29%). While inflation rose by 3.2% in March 2024, the 10-year average for March in the 2003-based index was 1.7%, indicating a favourable base effect this year. The data suggests that the currency depreciation in the second half of March did not have a significant impact.

PPI came in at 1.9% MoM, driven mainly by food products, textile and metals, while showing a drop annually to 23.5% YoY vs a month ago. The data indicates a notable weakening in cost pressures since mid-2024, largely due to currency stability, which in turn has contributed to a more favourable trend in Turkish lira-denominated import prices.

Core inflation (CPI-C) rose by 1.5% MoM, bringing the annual rate down to 37.4%. This downtrend, which has continued since mid-2024, has been supported by the relatively stable foreign exchange basket and the positive outlook for PPI. However, the impact of recent exchange rate movements is expected to be more visible in April. A preliminary assessment of seasonally adjusted data – set to be published by TurkStat tomorrow and closely monitored by the CBT to gauge underlying trends – reveals a mixed picture for March. While monthly headline inflation and goods inflation accelerated, core and services inflation showed improvement.

Inflation outlook (%)

Breaking down the data:

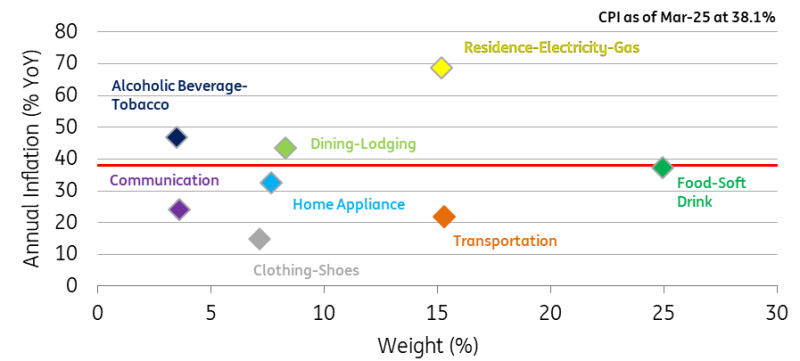

- The food sector was once again the biggest contributor to headline inflation, adding 1.23 percentage points. Monthly inflation in this sector reached its highest March level in the current inflation series, mainly due to rising unprocessed food prices.

- Alcoholic beverages & tobacco and housing followed, each contributing 0.33ppt. The rise in cigarette prices drove inflation in the former, while rent increases and higher water fees contributed to inflation in the latter. On a positive note, rent inflation slowed, with a MoM increase of less than 4%.

- Conversely, clothing helped reduce headline inflation by 0.15ppt, as we also saw in the previous month.

- Consequently, goods inflation remained steady at 30.5% YoY, while core goods inflation – generally considered a better indicator of the trend – fell below 20% YoY for the first time since November 2021.

- Services inflation, which is less affected by currency fluctuations but more influenced by domestic demand and minimum wage increases, continued to decline. It dropped to 56.3% YoY, marking the lowest level since summer 2022.

Annual inflation in expenditure groups

Overall, annual inflation declined further in March, aided by a favourable base effect, despite increases in food and tobacco prices. A higher FX trajectory in the near term following recent volatility, with a potential influence on inflation expectations, will likely weigh on the inflation outlook. These effects are likely to become more apparent in April. However, the CBT's policy measures should help mitigate some of the negative impact.

Given this context, disinflation is expected to continue, albeit at a slower pace than previously anticipated. In response to rapid market shifts, the CBT has implemented significant policies aimed at managing FX and inflation expectations, restoring market confidence, and addressing financial volatility. Additionally, the central bank also issued policy guidance signalling its readiness for further monetary tightening in the event of a sustained and substantial deterioration in inflation. Accordingly, we expect the bank to remain on hold in its April rate-setting meeting.

Download

Download snap