Czech industry slides as construction advances and wages pick up

Czech real industrial output slid in October, reflecting the havoc in European car manufacturing and the endless weakness of the German economy. Continued growth in new orders provides some sign of hope when looking ahead, with accelerating wages providing enough fuel for domestic spending to drive the economic rebound

Manufacturing output flirts with a downward trend

Czech real industrial production fell by 2.1% year-on-year in October when adjusted for the number of working days, partially due to the high comparison base of the previous year and notably for manufacturing of motor vehicles. At the same time, the adjusted industrial output shed 0.7% month-on-month in real terms. The value of new orders at current prices added 2.0% YoY in October, with new orders from abroad increasing 3.1% YoY and domestic new orders 0.2% YoY. However, the value of new orders was 0.5% lower than the previous month.

Industrial output under pressure in Czechia and Germany

The average number of employees in manufacturing decreased by 2.0% YoY in October. At the same time, the average monthly nominal wage in the industry accelerated to an annual growth of 7.2% in October. This represents an upbeat wage gain at the beginning of the year’s final quarter, providing a decent boost to household budgets at the year’s finish line.

Construction output fell by 3.6% YoY in October but was 3.8% higher than in the previous month. The indicative value of new building permits dropped by 17.6%, partially because of the preceding year’s high comparison base. However, 14.6% fewer dwellings were started compared to last October, and 48.4% fewer dwellings were completed. Given the rebound in demand and roaring appetite for property purchases, the mismatch between supply and demand will likely push property prices higher in the coming quarters and perhaps years.

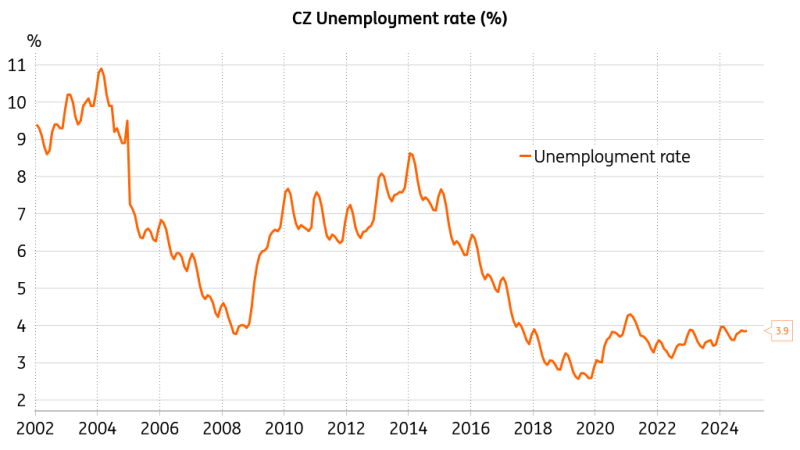

The average number of employees in construction was 2.1% below the last October's value, but the average monthly nominal wage accelerated to 10.1% YoY at the beginning of the last year’s quarter. According to the latest data from the Czech Ministry of Labor, the unemployment rate ticked only marginally higher to 3.9% in November, meaning that the labour market remains relatively tight. Moreover, the booming construction sector is about to absorb some of the workers laid off in manufacturing, especially when the winter comes to an end and construction activity takes off properly.

The labour market tightness drives wage growth

Overall, the Czech industry is not quite out of the woods yet, given the havoc in the European automotive sector and the endless weakness of German manufacturing. The continued annual growth in new orders provides some hope for the outlook. At the same time, the tight labour market keeps wage growth at lofty dynamics in both industry and construction, boosting household budgets and resources for further spending. The acceleration of wages in construction suggests a broad-based boom in the sector. Meanwhile, excess demand for residential properties will propel real estate prices in the coming quarters, and this will also be reflected in upward pressure on rents and core inflation.

Foreign trade gains pace

According to preliminary data, the balance of Czech foreign trade in goods at current prices ended in a surplus of CZK11.0bn in October, which was CZK3.2bn lower than the previous year. The overall balance of foreign trade in goods was favourably influenced in particular by a higher surplus in the motor vehicles segment. At the same time, the deficits in oil, natural gas, and chemicals narrowed noticeably.

Exports and imports continued to grow annually for the fourth month in a row. This time, however, the growth rate of imports exceeded that of exports. The gains in imports were related, among other things, to the pre-Christmas stocking. Exports in October gained 2.8% from the previous year, and imports added 3.7%. Also, in seasonally adjusted terms, exports increased by 1.1% and imports by 2.0% in October from the previous reading.

Download

Download snap