China’s CPI edged down to end the year

A fall in food prices dragged inflation lower, but a small uptick in non-food prices helped the headline stay barely positive

| 0.2% YoY |

China's 2024 CPI inflation |

Deflationary pressures persist as headline inflation fell

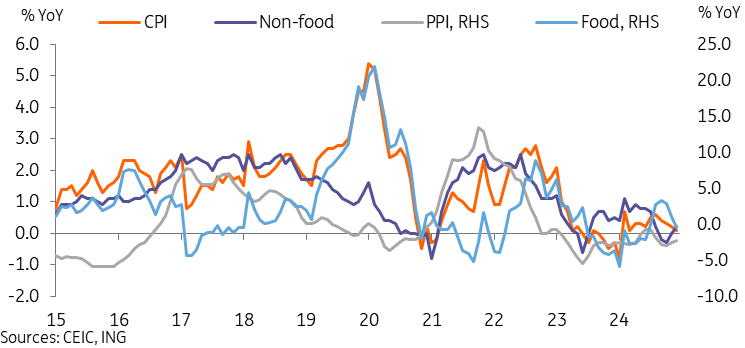

December CPI inflation edged down to 0.1% year-on-year, down from 0.2% YoY in November, and tying March 2024 for an 11-month low. Headline inflation has now gradually moved lower for four straight months. CPI inflation ends the year at 0.2% YoY, lower than forecasts for most of the year.

The main drag on inflation in December came from food prices, which fell to a six-month low of -0.5% YoY. China's pork cycle looks to have started its downturn, with pork prices down -2.1% month-on-month, the third consecutive month of sequential declines. While the YoY gauge is still in double digits at 12.5%, it is no longer enough to keep food inflation positive. Additionally, we saw fresh vegetable prices fall -2.4% MoM, bringing the YoY gauge to just 0.5%. Various other food categories, including beef, dairy, fruits, grains, and oils, are already in YoY deflation.

December's headline number managed to avoid falling into deflation thanks to non-food inflation, which returned to slight positive territory at 0.2% YoY, after spending the last three months at 0% or in deflation. However, the breakdown of non-food prices also does not inspire too much confidence in an uptick of consumption yet; the gains mostly came from clothing (1.2%), education (1.2%) and healthcare (0.9%) prices, while we saw continued deflation in transportation and communications (-2.2%) and daily use goods (-0.7%), and rent (-0.3%).

Finally, PPI inflation unsurprisingly remained in deflation for the 27th consecutive month, but saw a slightly smaller contraction at -2.3% YoY.

Uptick in non-food prices staved off headline deflation for another month

Continued low inflation further bolsters the case for further monetary easing

It is likely that the upcoming Lunar New Year will help January inflation rebound, but overall inflation is expected to remain low in 2025.

The People's Bank of China has been signalling further easing for some time; we don’t think the CPI is likely to be the main catalyst in terms of timing, instead the PBoC may choose to wait for tariff announcements or a month of weaker-than-expected activity data to get the most value out of a cut.

With that said, the continued weak inflation certainly adds to what is already a favourable case for more rate cuts, and policymakers have already signalled a "moderately loose" monetary policy stance for 2025. We are expecting a rate cut as well as a reserve requirement ratio cut in 1Q25.

Download

Download snap