Bank Pulse: January bank lending volume down, rates slightly up

In the aftermath of the targeted longer-term refinancing operations (TLTRO), January bank lending to business dipped. Meanwhile, rates crept up marginally

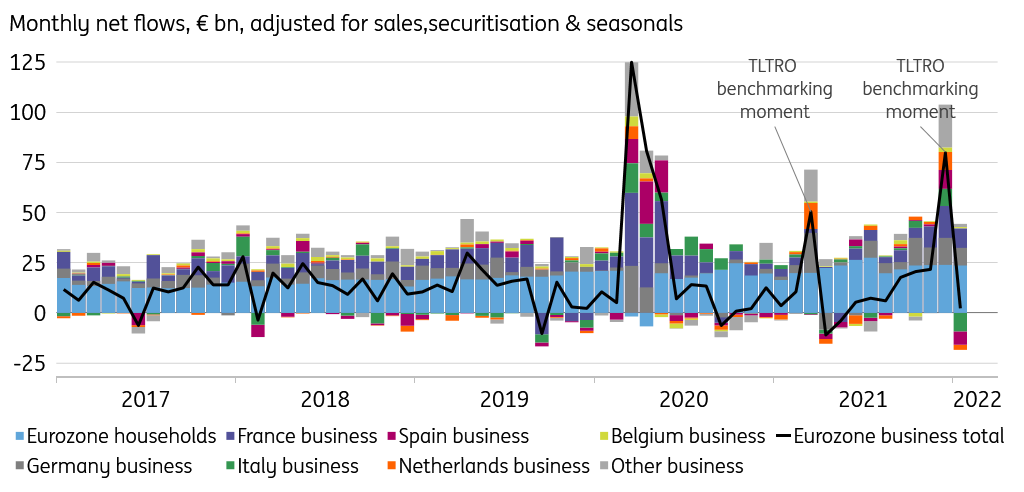

Back in December, eurozone bank lending to businesses peaked as banks scrambled to meet their TLTRO lending benchmark. This is corroborated by the fact that both in absolute and relative terms, most of the year-end sprint in lending was realised in the above €1m segment, in contrast to the Spring 2020 lending spike, which was much more evenly spread across loan sizes.

Some of the year-end lending no doubt included front-loading, so a dip in January bank lending to business was to be expected, similar to what happened last March and April, around the previous benchmark assessment deadline (see chart). Indeed, January bank lending to businesses dipped in several countries, though notably not so much in France and Germany, indicating resilient business borrowing demand there. The ECB Bank Lending Survey did show slightly stronger borrowing demand in these countries compared to Italy and especially Spain.

Eurozone bank lending to households and non-financial businesses

Business borrowing rates edged back up in January in most of the large eurozone economies, but this should not be misread as the early sign of an emerging upward trend. Rather, the January increase comes on the heels of rate decreases in November and December. Some banks have likely been offering rate discounts to generate the lending volume necessary to meet their TLTRO benchmark. In any case, at a eurozone average of 1.43%, rates remained historically low in January.

Lending growth to households is not in scope of TLTRO and net volumes have remained virtually unchanged since October. Meanwhile, eurozone average household borrowing rates increased marginally to 1.84%. Yet looking through normal seasonal fluctuations, rate changes were negligible, and rates have been moving sideways for a few months in a row now.

We previously expected a slow but steady upward drift in borrowing rates in the course of this year, on the back of the European Central Bank monetary policy normalisation and policy rate hikes appearing on the horizon. Obviously, with the war in Ukraine, everything has been thrown into doubt. The ECB’s monetary response will largely drive the direction of bank lending rates in the months ahead. We do think that at next Thursday’s ECB meeting, the previously made commitments around ending the pandemic emergency purchase programme (PEPP) this month (while continuing reinvestments) and increasing the asset purchase programme (APP) from April will hold, but we don’t think the ECB will commit to a clear path of tightening next week before knowing more about the economic impact of the crisis. Given that the short-term direct financial spillovers to eurozone banks appear manageable, we don’t currently expect the ECB to make any announcement on a new round of its targeted longer-term refinancing operations or other liquidity-enhancing modification to the programme.

The development of business borrowing demand in the months ahead is highly dependent on the economic effects of the war in Ukraine, including declining exports to Russia and Ukraine, higher energy prices and possible supply chain disruptions and wider confidence effects.

Download

Download snap