US: Waiting for lift-off

The economy will likely continue struggling for the next month or two, but with vaccinations accelerating and households looking cash rich a reopening of the economy could see growth reach multi-decade highs

The quicker the vaccinations the sooner the reopening

The US economy started 2021 on a weak footing following three consecutive monthly falls in retail sales at the end of the year and news that 140,000 jobs were lost in December. With Covid containment measures continuing to weigh on sentiment and activity, we suspect that the economy will struggle through much of the first quarter.

However, the outlook thereafter is undoubtedly brightening. The US is getting close to averaging one million Covid vaccination doses a day with President Biden promising more resources to ramp up the process to 1.5 million and possibly even 2 million per day. With the warmer weather of spring approaching and hospitalisation numbers already falling, there is hope that a second quarter reopening of the economy is possible.

Covid cases and hospitalisations are falling. Deaths will follow

Consumer boom

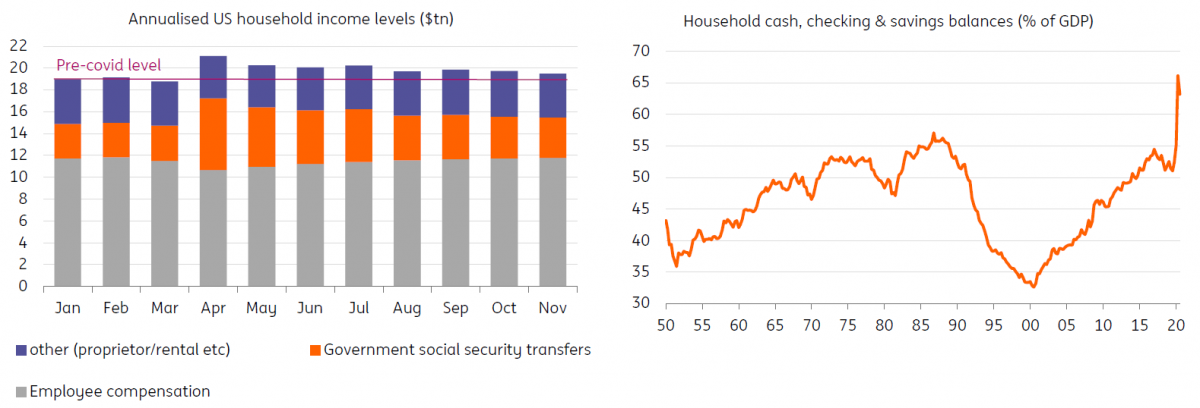

We expect to see consumer spending leading the charge with pent-up demand focused on the leisure, travel and entertainment sectors. Households are cash rich with government support programmes (extended unemployment benefits and individual cheques) helping lower income households. At the same time, the inability to travel and spend money on “experiences” has led to involuntary saving by higher income groups. The result is that savings in cash, checking and time deposits have surged $2.4 trillion between the third quarter of 2019 and third quarter of 2020.

More support is proposed with a $1.9tn fiscal plan set to make its way through Congress although some dilution and modifications will likely be required to get it passed.

With credit card balances at four-year lows this means there is a huge amount of cash ammunition with which to propel spending higher. Add in the prospect of significant employment gains as the downtrodden service sector finds its feet and 2021 looks set to be the strongest year for economic growth in decades.

Elsewhere, the buoyant housing market is likely to keep residential construction activity robust while capex by US corporates is likely to recover after 12 months of flatlining. A pick-up in global trade and a more internationally-competitive US dollar following its recent declines will also support activity.

Higher household incomes have boosted savings

Inflation set to rise

Inflation will inevitably move higher. Much of it will be base effects as price levels in a vibrant, reopened economy will be higher than they were when companies were desperate for cash and were slashing prices in the depths of the pandemic in 2Q 2020. Moreover, higher fuel prices and some capacity constraints in heavily distressed sectors will add to upside inflation risks in the near-term.

Given this reflationary environment we expect to hear more talk of potential quantitative easing tapering this year with Federal Reserve interest rate hike expectations forecast to creep forward to 2023 from 2024.

Market inflation expectations have jumped

Can we avoid a taper tantrum?

This runs the risk of a taper tantrum 2.0 – similarly to when the Fed signalled it was going to slow its QE purchases in 2013 and the 10Y Treasury yield jumped from 1.6% to 3%. If repeated, this would lead to disruptive moves on the cost and availability of domestic credit, with implications for broader asset classes, including emerging markets.

We suspect that the tapering will be gradual and is likely to involve a twist operation to start – cutting the total purchases, but weighting more of those purchases towards the long end of the yield curve. Volatility could be further reduced if the Fed signals they are prepared to be flexible on this taper, such as by being willing to halt the taper and even temporarily increase purchases, depending on market circumstances. With more debt issuance coming this could be an important way of calming the market.

Fiscal optimism, but remember the mid-terms

The next move in fiscal policy will be an attempt to pass Joe Biden’s $3tn+ Build Back Better infrastructure and energy plan. This is going to be a major challenge given the Republican Party’s re-discovered fiscal conservatism and the Democrats tiny majorities in the House and Senate.

The clock is already ticking given the mid-term elections in 2022. With all House seats and a third of the Senate up for re-election, legislation will have to be accelerated to give it time to be passed by Congress. Remember that through the 20th century, the incumbent President’s party has on average lost 26 House seats and 4 Senate seats at the mid-terms. If this were to be repeated, the Republicans would control Congress and Joe Biden would be a lame duck President in the final two years of his term, with little chance of getting any more of his proposals written into law.

Download

Download article

29 January 2021

Hopes fade for a synchronised global recovery This bundle contains 10 articles

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more