The May commodities rally comes to an abrupt end

Oil is down, and so is copper after hitting record highs in May. Natural gas prices, however, continue to be supported by supply concerns

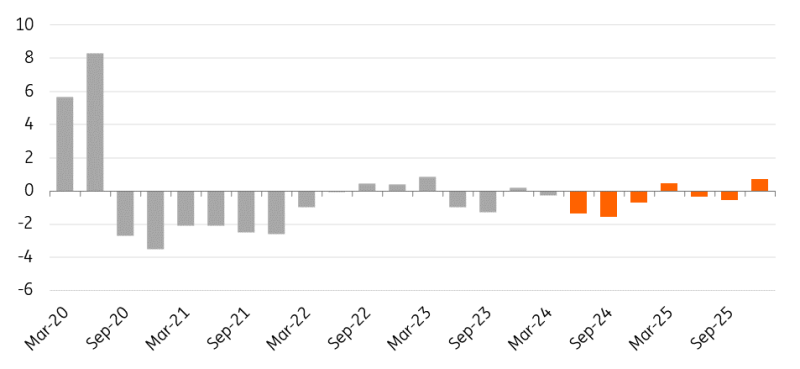

Oil market in deficit for the remainder of 2024

Oil prices were largely rangebound through much of May but have come under pressure in recent days. There are growing signs of weakness in the physical oil market, which prevented oil prices from moving significantly higher. Weak refinery margins are starting to see refiners reducing run rates, while the weakness in prompt crude oil timespreads suggests little concern over the availability in the near term.

The easing in oil prices will be a concern for OPEC+, and it's no surprise that the group decided at its 2 June meeting to extend their additional voluntary supply cuts of 2.2m b/d until the end of September 2024. Members will then start to unwind these cuts gradually from October through to September 2025. Meanwhile, group-wide cuts of around 2m b/d, which were set to expire at the end of 2024, have been extended to the end of the following year. 1.66m b/d of voluntary cuts, which have been in place since May 2023, will similarly be extended to the end of 2025.

Action taken by OPEC+ should ensure that the market remains in deficit for the remainder of the year and that should provide support to oil prices during the peak demand period over the summer months.

However, we would expect oil prices to ease through 2025 from a peak in the third quarter of this year, with the market set to return to a small surplus as OPEC+ gradually returns supply to the market. There is potential that OPEC+ decides against unwinding cuts if market conditions do not allow for additional supply. However, longer term, the scale of cuts from the group could become an issue. Members will likely grow frustrated by holding a significant amount of oil from the market and giving market share to non-OPEC+ producers.

Oil market in deficit for the rest of 2024 before returning to surplus in 2025 (m b/d)

Supply worries boost European natural gas

European natural gas prices have strengthened significantly over the last month. TTF has rallied almost 18% in May, taking prices above EUR34/MWh. Several supply concerns have driven the market higher.

Firstly, ongoing summer maintenance in Norway has reduced Norwegian flows to Europe. In May, daily average flows were 8% lower month-on-month. More recently, an unplanned outage in Norway due to a crack in a pipeline led to even lower pipeline flows, only intensifying supply concerns and adding to volatility.

Secondly, Asian LNG demand has been stronger so far this year. LNG imports in the first five months of 2024 were up 11% year-on-year. Stronger demand has been driven by hotter weather in large parts of Asia and we have also seen more price-sensitive buyers in the region returning to the LNG market, with spot prices coming down from the high levels seen in 2022 and 2023.

And there are still concerns over the remaining Russian pipeline flows to the EU, specifically those to Austria. The Austrian oil and gas company OMV announced there is a risk to Gazprom supplies to the country following a court case ruling which could block payment to Gazprom for gas deliveries. If enforced, it would likely lead to Gazprom halting those flows. OMV has a long-term contract of around 6bcm per year for Gazprom supplies. However, Austria and Europe as a whole should manage if this supply is lost. In addition, from late 2024 onwards, a large amount of new LNG supply capacity is scheduled to start, largely from the US.

The likelihood that Russian pipeline flows to the EU via Ukraine come to a stop at the end of this year is also high; Ukraine has made it clear that it has no intention to extend a transit deal with Gazprom. This would mean the loss of around 15bcm of gas, which is around 5% of total EU imports. While Gazprom may be able to divert some marginal flows via TurkStream, Europe would need to look for alternative supplies. That potential supply loss has moved from a risk to the market to probably being largely expected.

Despite numerous concerns, Europe should see storage hitting 100% full ahead of the 2024/25 heating season. It's already more than 71% full, well above the five-year average of 59%, and also slightly ahead of last year’s level of 70%. As a result, we continue to expect European gas prices to weaken over the third quarter of this year.

Copper hits record levels

Metals stood out in May, leading the complex higher. Copper prices rallied more than 10% last month, reaching a new record high of more than $11,000/t. However, since then, prices have given back a lot of these gains. The move in copper has been driven by speculators with a bullish narrative due to concerns over a lack of mine supply at a time when demand is set to grow strongly amid the energy transition. In addition, several support measures announced over the last month for the Chinese property sector added to the positive sentiment.

However, while the longer-term outlook remains constructive for copper, short-term fundamentals are still a concern, particularly in China. Copper stocks held in Shanghai Futures Exchange (SHFE) warehouses are at seasonal record highs. Chinese import premiums for refined copper are negative, and domestic refined copper output continues to grow year-on-year despite treatment charges falling significantly for smelters.

Furthermore, LME copper stocks have grown more than 15% since mid-May, while the cash-3-month spread is in deep contango and not far away from the recent record lows – suggesting little concern over refined copper supply in the near term.

Download

Download article

7 June 2024

ING Monthly: All eyes on Europe This bundle contains 13 articlesThis publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more