Back to black: the countries best positioned to replace Russian gas with coal

European countries are being forced to revive coal plants to cut back their dependency on Russian gas. Poland and Germany are in the best position for that gas-to-coal switch. Moving to more nuclear power will be tricky for many others. And we have to consider the environmental concerns

Coal and nuclear power plants might come to the rescue

Gas flows from Russia to Europe have been reduced to alarmingly low levels in recent days. On top of that, the LNG market is also tighter following an outage at the Freeport LNG export terminal in the US.

This has fuelled debate about how to reduce gas use in the EU. Previously we concluded that there is no silver bullet for sectors, but the power sector could play an important role. In this article, we look at to what extent the power sector can substitute gas-fired power plants with coal-fired plants (gas-to-coal switch) or nuclear power plants (gas-to-nuke switch).

Our main conclusions are:

-

Poland, and to a lesser extent Germany, can substitute gas use by gas-fired power plants by running coal plants at full capacity, provided that enough coal is available.

-

The Netherlands lifted the 35% production cap for coal plants which could substitute 46% of gas-fired power generation, if the four remaining coal plants are fully utilised.

-

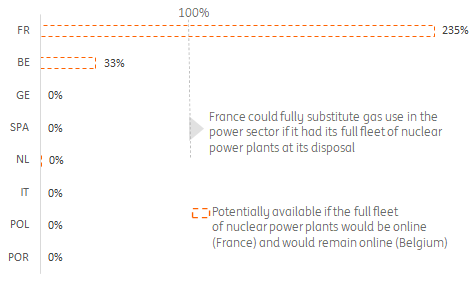

France could fully substitute gas use in the power sector if it had its full fleet of nuclear power plants at its disposal. Unfortunately it has not, as 24 of the 56 nuclear reactors are shut down for maintenance. Hence, there is no room for a gas-to-nuclear switch.

-

Belgium could substitute one-third of gas use in gas-fired power plants by running the current seven reactors at full capacity. That is unlikely to happen as two reactors will be closed soon, one in 2022 and one in 2023. Without these reactors, there is no potential to substitute power from gas plants with power from nuclear plants. The decision to extend the life cycle of two of the remaining five reactors does not change that outcome.

-

The closure of the three remaining nuclear power plants in Germany later this year has eliminated the option for a gas-to-nuclear switch in the country.

We arrived at these conclusions by looking at the extra power generation from coal and nuclear-fired power plants for a set of European countries if these plants are fully utilised – that is if they run at full capacity – and provided that there is enough coal available. More details on this theoretical exercise can be found in the box at the bottom of this page.

Coal plants: burn baby burn

Current energy markets provide favourable economic conditions for coal-fired power generation. The so-called dark spread is a measure of the competitiveness of coal-fired power generation compared to gas-fired power generation and shows high-profit levels for coal plants.

But despite favourable economic conditions, coal plants are generating less than they can. Coal-fired power plants have been closed recently or were restricted to run at full capacity as a result of climate and energy transition policies.

Our analysis suggests that gas use from gas-fired power plants can be fully substituted by coal-fired power plants in Poland and Germany and to a very large degree in Portugal, Spain, and the Netherlands. In these countries, coal is an ‘easy’ answer to addressing energy security risks, despite the fact that it goes against global climate goals.

Poland and Germany could fully substitute gas use in the power sector by increasing coal-fired power generation

Potential extra coal-fired power generation as a percentage of current gas-fired power generation

Poland is the first European country that managed to top up its gas storage facilities. They are now 81% full as Poland was able to source a lot of LNG. Still, the 3.2 billion cubic metres (bcm) of stored gas is only a fraction of domestic gas consumption, at 21.3 bcm. The country is still vulnerable to prolonged gas disruptions.

Poland’s power mix is highly dependent on coal as the country started to switch to gas relatively late. According to Bloomberg New Energy Finance (BNEF), the share of coal-fired power generation has come down from 94% in 2000 to 72% in 2020 on the back of more power generation from renewables and gas-fired power plants. Still, available coal capacity has not changed in the past 20 years and stands at ~30 gigawatts. By running coal plants at full capacity, Poland could easily phase out gas use in its gas plants.

Our analysis yields the highest number for Poland, at a stunning 230%. So if the country runs its coal plants at the maximum level seen in the past 20 years, it would generate an additional amount of coal power that is 230% higher than the power it currently generates from gas-fired power plants. With ample capacity, it might have room to export coal power to neighbouring countries to facilitate them in their pursuit to reduce gas dependency.

The intuitive answer to why this number is so high in Poland is easy: the fleet of coal-fired power plants is so much bigger than the fleet of gas-fired power plants, so it is relatively easy to substitute power and gas from gas plants.

However, this can only be used if enough coal is available. Currently, coal is scarce in Poland due to the embargo on Russian coal and under-investment by coal companies.

The German coalition intends to phase out coal plants in 2030 instead of 2038 when it entered office in November 2021. A gradual phase-out of lignite and hard coal power plants has already been started with Germany having run five ‘coal closer auctions’ so far in which owners of coal plants can bid on compensation for shutting down their power stations. Germany's coal exit laws set a 15 GW maximum capacity target each for lignite and hard coal, with lignite closures following a set timetable. The most recent closures, however, have now been reversed due to the potential scarcity of natural gas arising from the Ukraine crisis.

If Germany fully utilises all of its coal plants, including the coal plants in the power reserve markets, it would generate around 100% more power than it produces with gas-fired power plants. In other words: it could substitute gas use from gas-fired power plants entirely, provided there is enough coal available. If one excludes the coal plants in the power reserve markets, the number drops to 59%.

The Netherlands operates four coal-fired power plants of which three are relatively large and new. The Dutch Urgenda court law required the Dutch government to lower emissions by 25% by 2020 onwards. In order to reach this target, the output of coal plants in 2022 was capped at 35% of full potential for 2022. This cap has been lifted as of 20 June, so that coal plants can substitute up to 46% of the gas use in gas-fired power plants, which are the dominant source in the Dutch power system.

Nuclear power plants; maintenance issues and plant closures prevent full utilisation

France is Europe’s nuclear powerhouse with 56 operational nuclear power plants adding up to a whopping 64 gigawatts of capacity. In normal times these reactors meet more than 70% of the power demand in France. If these nuclear power plants ran at full capacity, France could very easily replace more than two times the amount of gas it needs for its gas-fired power plants.

But unfortunately, these are not normal times. Since 2015, France’s nuclear capacity has fallen. This drop is partly explained by the closure of the Fessenheim reactor in 2020, but mostly it is caused by maintenance work and unscheduled interruptions. Currently, 24 of the 56 nuclear reactors are shut down for maintenance and just 30 gigawatt is available. As a result, power prices in France have reached historic highs.

Most maintenance has to do with the refuelling of reactors that needs to be done every one or two years, and these reactors will come online soon. But some reactors need to be welded as a result of longer-term overhauls. There are also unplanned outages due to an unseasonably warm May. River water is often used for cooling reactors before being returned to the river at a higher temperature. Regulations are in place that restrict the use of cooling water in order to prevent damaging local wildlife.

EDF, the state-owned operator of the reactors, is constantly updating its maintenance schedule for the fleet. EDF might be able to postpone maintenance at some plants until after the winter, but it is unlikely to bring back enough capacity to replace gas use in gas-fired power plants any time soon.

France could fully substitute gas use in the power sector if it had its full nuclear fleet at its disposal

Potential extra nuclear power generation as a percentage of current gas-fired power generation

In Belgium, French utility Engie operates seven nuclear plants; four in Doel and three in Tihange. In accordance with the current law, it will proceed with the shutdown of these between 2022 and 2025: Doel 3 in 2022, Tihange 2 in 2023, and the other reactors in 2025. Their shutdown will be followed by their decommissioning and dismantling, which is set to be completed by 2040.

With all seven nuclear plants running at full capacity, Belgium could save up to a third of the gas used in gas-fired power plants. But without the Doel 3 and Tihange 2 reactors – which together account for two gigawatts of nuclear capacity – there is no potential to save on gas in gas plants by running the five remaining nuclear plants at full capacity.

The Belgium government, in a bid to alleviate the energy crisis, has recently said it plans to keep two reactors, known as Doel 4 and Tihange 3, running for another 10 years. Engie responded by saying that the decision to extend the operational lifetime of the reactors raises "significant safety, regulatory and implementation constraints" as maintenance has been scaled down in recent years in anticipation of the forced closure. And it still implies the closure of Doel 3 in 2022 and Tihange 2 in 2023, leaving no room to save gas in gas plants by maximising power generation in nuclear plants.

Shortly after the Fukushima disaster in 2011, Germany decided to phase out its nuclear fleet (called the ‘Atomausstieg’). Three nuclear power plants remain active, down from 17 in 2011, and they’re scheduled for decommissioning at the end of this year. Three other plants that closed at the end of 2021 are in the early stages of a shutdown. All other plants are being dismantled, and can’t just be switched back on.

The war prompted the government to run an assessment in March on whether it should and could delay the phaseout in light of the energy crisis. So far, the government is sticking to the current plan to close the remaining reactors by the end of the year, due to technical, legal, political, and security objections to lifetime extension. Recently, however, some members of the government publicly advocated the option to at least look into an extension.

Any realistic discussion about delaying the phaseout centers around the three remaining plants in operation that are scheduled for closure this year. It is interesting to see that Japan is currently considering a reignition of reactors that were shut down after the Fukushima disaster. Bringing back to life the three plants that were recently closed does not seem to be a realistic option for Germany, at least for now. The three plants that are still running hardly provide room for a gas-to-nuclear switch.

All in all, maintenance issues in France and the phase-out of nuclear power plants in Belgium and Germany have eliminated the potential of a gas-to-nuclear switch in the European Union.

Increasing coal use comes with climate risks

It is often said that saving gas by increasing coal use raises emissions in the power sector as coal-fired power plants emit twice as much carbon as gas-fired power plants; it feels like the wrong thing to do for the climate.

However, the power sector is part of the emissions trading scheme (ETS) in the EU. That means that, on an EU level, the combined emissions of the power and manufacturing sector are capped and are being reduced in accordance with emission reduction goals. The current cap ensures 40% fewer emissions by 2030. And the Fitfor55 package raises the bar to 55% in order to set the EU on a trajectory to net-zero by 2050.

As such, decisions to lower or increase coal-fired power generation do not impact the total carbon emissions for the ‘ETS sectors’ towards 2030. So, some might say that turning on coal plants isn't necessarily a climate disaster.

The ETS carbon price makes sure that companies will lower their emissions according to the emission reduction goals. So far, the reaction in the EU carbon market has been muted on news of the use of more coal plants. After all, emission levels in the power sector might rise, but emissions in manufacturing are likely to drop as a result of the curtailment of production from high gas prices.

This stands in sharp contrast to the market reaction in the run-up to the Fitfor55 package. Raising the bar in the ETS did indeed result in much higher carbon prices. These market reactions could be viewed as clear signs that carbon pricing is working in the sectors currently covered by the ETS. If Europe is serious about lowering carbon emissions, it should ratify the Fitfor55 proposal and not be too specific about fossil fuel technologies to get there.

While increased coal use does not seem to jeopardise the emission reduction targets for Europe, the situation is less positive on a global level. Asia, for example, is also suffering from high gas prices and increasing coal production, but carbon markets are less advanced in this part of the world. As long as there is no single global carbon market, or as long as regional carbon markets are poorly interconnected, raising global coal production is not a good sign for global carbon emissions and hence global warming. The response of heavy coal users like China and India to the energy crisis will be crucial.

Our methodology: calculating the potential of a gas-to-coal and gas-to-nuclear switch

We have analysed 20 years of power market data from BNEF for the countries involved, from 2000 up to 2020, so that results are not impacted by drops in power demand from the Covid-19 lockdowns. We looked at both capacity and generation data for all the different technologies in a country’s power mix (coal, gas, nuclear, renewables, etc). By analysing historic load factors (the amount of power generation per unit of installed capacity), we were able to get a feel for the cyclical variation of load factors for coal and nuclear power plants driven by energy market conditions. We defined the upper range of the load factor as a proxy for a technology's full potential and applied it to the current available capacity of that technology in the market.

This results in the power generation from coal or nuclear capacity if it would run on the highest load factors seen in the past 20 years, and provided that there is enough coal available to fully utilise coal plants and enough cooling water to run nuclear plants. We compared the increase in power generation with actual power generation and calculated to what extent that extra power could replace power generation from gas-fired power plants.

While this analysis yields useful insights it has the following shortcomings:

- We looked at annual data but that does not guarantee that seasonal patterns in power demand or during peak hours can be met. There might be problems in assuring adequate capacity in order to manage electricity in peak hours. Gas plants are typically used to balance the grid and satisfy demand in peak hours. A switch to less flexible coal and/or nuclear power generation is likely to require more ‘demand-side management policies’.

- We only looked at gas use in the power sector, but electricity only accounts for one-fifth of energy demand in the EU. Half of the energy is used for heating and gas is an important energy source to generate heat. As such, real estate and manufacturing are also important sectors to limit gas demand.

- We took a short-term horizon to look for solutions in the power sector to save on gas so that energy security risks can be addressed. And with high gas prices, it might also serve the goal of an affordable energy system. The transition towards a net-zero economy is obviously the main long-term goal (sustainability). Electrification is key for decarbonisation in transportation, manufacturing, and real estate. In many countries, power demand is expected to increase strongly by 2030 (many models predict a rise of +50 to +100% by 2030). Our analysis ignores the important topic of how to meet an increasing power demand within heavily constrained power grids.

Download

Download article

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more