Russia-Ukraine conflict: What it means for grain and oilseed markets

The sad events we are seeing in Ukraine have brought the issue of food security to centre stage. Disruptions to supply chains along with self-sanctioning has pushed grain prices to multi-year highs. Given the importance of Russia and Ukraine to grain markets, uncertainty over the supply outlook means prices will remain elevated and volatile

The importance of Russia and Ukraine to agri markets

You do not need to look much beyond the recent price trends in grain and oilseed markets to know the importance of Russia and Ukraine to global markets. CBOT wheat has rallied by more than 70% this year, with prices breaking above US$13/bu and trading to its highest levels since 2008. Corn has also seen strength, rallying almost 30% this year and taking it to levels last seen back in 2013. Finally, soybeans have rallied by more than 25%, breaking above US$17/bu at one stage – levels not seen since 2012. Admittedly, the strength in soybeans would be largely due to crop downgrades in South America, but there will also be support from a tight palm oil market, as well as concerns over sunflower oil supply from Ukraine and to a lesser extent Russia.

The ongoing uncertainty suggests that grains and oilseed markets will continue to price in a significant risk premium. Lost export supply from Ukraine and Russia would tighten up global wheat and corn balances significantly, and as a result change the outlook for at least the next season.

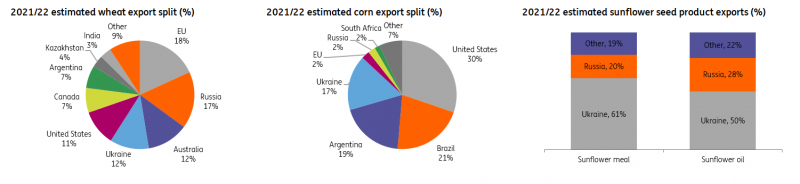

Russia & Ukraine- powerhouses when it comes to grains

Ukraine is a significant producer of grains. In 2021/22 it is estimated to produce 42mt of corn according to the USDA, and expectations were for exports to total 33.5mt. This would have left Ukraine making up around 17% of global export supply and taking the spot as the world’s fourth largest corn exporter.

Similarly, when it comes to wheat, Ukraine is also a large producer. The USDA estimated it to produce 33mt in 2021/22, whilst exports were expected to total 24mt. This would have left Ukraine as the third largest exporter, holding a share of almost 12% in the global export market.

Moving away from grains and focusing on oilseeds, Ukraine is the largest sunflower seed producer, with the USDA estimating 2021/22 output of 17.5mt, which accounts for more than 30% of global output. It also has a large domestic crushing industry, of which sizeable volumes of both sunflower meal and oil are exported.

In 2021/22 Russia is estimated to have produced 75.5mt of wheat, although has produced in excess of 85mt in recent years. Exports are estimated to total around 35mt this season, which would leave Russia as the largest exporting country, holding almost 17% of global export supply. As for corn, Russia is a less dominant supplier. Domestic output was estimated to total around 15mt in 2021/22, whilst exports were expected to finish the season at 4.5mt.

Russia is also the second largest sunflower seed producer, making up 27% of global output. Like Ukraine, most of this will be processed domestically, and any exports are in the form of oil and meal.

Russia and Ukraine are large exporters of grain and sunflower seed products

The Ukrainian impact

The concerns over Ukraine will be largely related to domestic production as well as disruptions to export flows. Ukrainian ports are shut, and according to Ukraine's Maritime Administration will likely remain shut until the conflict ends. Although even once the conflict eases, there may still be some hesitancy by shipowners to dock at these Black Sea ports, whilst insurers may also be reluctant to provide the necessary insurance.

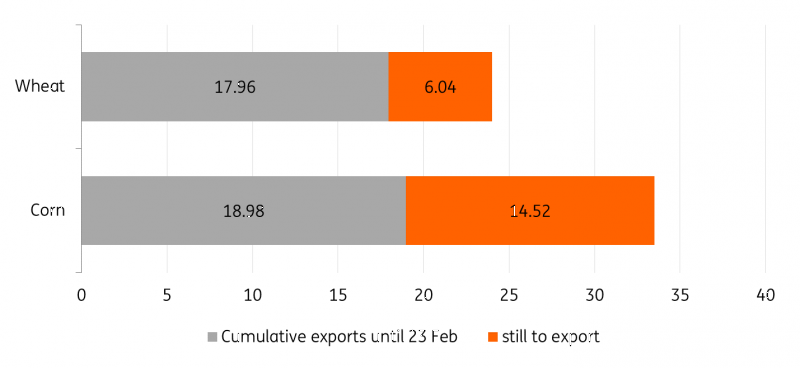

According to the latest data from the Ukrainian Agricultural ministry, cumulative wheat exports in the 2021/22 season stood at 17.96mt as of the 23 February. It is safe to assume that this number has not increased significantly since then. Given that exports were excepted to total 24mt this season, Ukraine still has about 25% to be exported between now and the end of June. This will be difficult given the ongoing conflict.

In addition, 2022 winter wheat is in the ground, and the ongoing conflict could very well disrupt husbandry and the application of necessary fertilizers. Therefore, assuming the conflict ends before the 2022/23 harvest starts in July, we could still see lower yields impacting output next season. In addition, if the conflict persists, there is the potential that not all area will be harvested for the upcoming season.

As for Ukrainian corn, there is still a sizeable amount of the 2021/22 crop to be exported. According to government data, Ukraine had exported 18.98mt of corn as of the 23 February. Like wheat, it is unlikely that this has increased much since then. Given that exports were expected to total 33.5mt this season, there is still about 43% to be shipped before the end of June. There is a risk that a large share of this will not make it to market.

The supply risk for corn potentially runs into the next season as well. Spring planting season is just around the corner, and if the current conflict continues into late spring, it is difficult not to see a large downward impact on corn plantings for the 2022/23 season. Sunflower seed faces the same risks as corn for the 2022/23 crop, with planting potentially delayed and significantly lower.

Ukraine still has a sizeable amount of grains from 2021/22 to export (m tonnes)

The Russian impact

The issue with Russia which is concerning markets is the self- sanctioning we are seeing with Russian commodities. The risk of additional sanctions against Russia appears to have made buyers reluctant to commit to Russian supply. There is also likely an element of reputational risk at the moment for some buyers. In addition, banks are less willing to finance the trade in Russian commodities, which will further weigh on Russian supply making its way onto the global market.

It is more difficult to assess the degree and as a result the impact of self-sanctioning. We are seeing it across commodities, where trade is taking a hit. However, when it comes to food, one does need to think about food security. So, whilst we may see a demand shock in the short term for Russian grain, it may not be sustainable, as key consuming nations will start to get increasingly worried about food inflation and the potential unrest this could cause. We just need to look back to the Arab Spring to see the impact of rising food prices. In addition, it would be unlikely that food would be included in sanctions, if we were to see further rounds of broader sanctions.

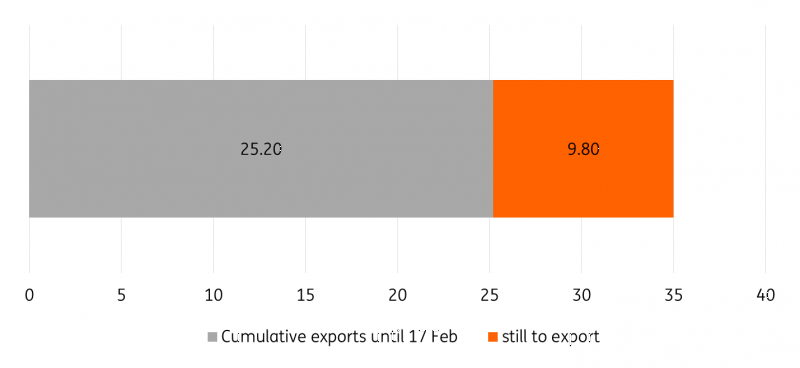

The latest available government data shows that Russia exported 25.2mt of wheat in the 2021/22 season through until 17 February, which leaves about 28% of the crop to still export this season, assuming an export number of 35mt for the full season. Russian shipments since the war will be holding up better than Ukrainian shipments, however given the self-sanctioning the pace has likely slowed.

Looking further ahead, if Russian commodities continue to be self-sanctioned, we could start to see farmers reacting by reducing area. For winter wheat it would be too late, however for spring wheat and corn there is the potential that the ongoing uncertainty leads to reduced plantings.

Self-sanctioning of Russian commodities likely to slow pace of 2021/22 wheat exports (m tonnes)

Changing trade flows and the potential for substitution

The supply disruptions have raised concerns over food security. We will likely see stronger buying from key consumers to ensure adequate supply if these disruptions persist. Already, China has ordered its appropriate agencies to ensure sufficient supply amid the current uncertainty. Key importers in the Middle East and North Africa will likely also want to ensure they are sitting on adequate inventories, wanting to avoid a repeat of the Arab Spring that we saw at the beginning of the last decade.

This will push buyers to look at other origins in order to ensure supply. Historically, China has been a large buyer of Ukrainian corn. China imported 8.2mt from Ukraine in 2021, which was about 30% of total Chinese imports. We are likely to see China turning increasingly to the US to make up for any shortfalls, much like we have seen in the last couple of years.

As for wheat, China has already made adjustments by lifting all restrictions on Russian wheat. Previously Russian imports were restricted due to phytosanitary concerns. China will likely be a home for a range of other Russian commodities, given that China is unlikely to follow any Western sanctions.

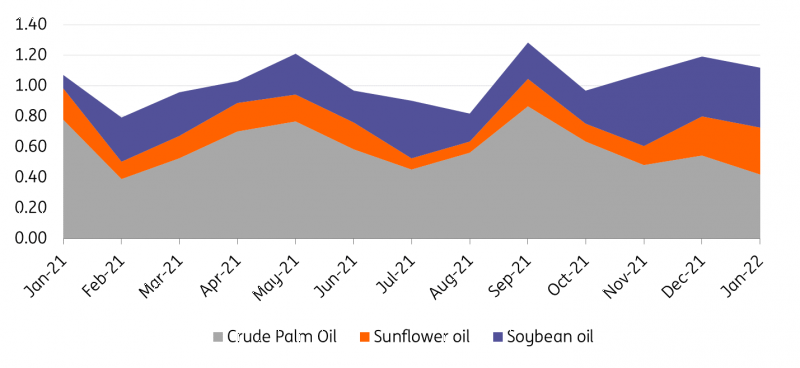

The vegetable oil market could potentially see increased substitution if disruptions persist. Although the issues with Ukrainian and Russian supply are coming at a time when there is already tightness in some of the other markets including palm oil. As a result, we could see more substitution towards soybean oil, which again would be positive for soybean crushers and ultimately soybean prices. This is a trend that we have already seen recently from the world’s largest vegetable oil importer, India, due to tightness in the palm oil market. This trend is likely to strengthen given the potential disruptions from Ukraine and Russia in sunflower oil now.

India vegetable oil imports could see even more of a move towards soybean oil (m tonnes)

Expect strong spring plantings from the US

Given that grains and soybeans are trading at multi-year highs, we would expect to see strong plantings from US farmers over the spring, leaving the potential for an increase in US spring wheat, corn and soybean area. This was already expected for all wheat and soybean area prior to the Russia-Ukraine conflict. But given latest developments we could see corn compete more aggressively for area. Although, farmers will take into consideration the higher input costs seen, particularly for fertilizer, when finalizing their planting intentions. The USDA will release its prospective planting report at the end of March which will shed more light on what farmers may do.

If we see a prolonged disruption in supply from Ukraine and Russia, increased plantings from other producing countries may help, but clearly will not offset the full potential losses from these Black Sea producers. Under such a scenario, global balances will tighten, providing support to prices. However, for now expect markets to remain volatile.

Download

Download article

11 March 2022

A global power struggle This bundle contains 9 articlesThis publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more