Robust underlying growth despite US GDP disappointment

US GDP expanded “only” 2.3% in the fourth quarter, but this masks consumer strength via a big run down in inventories and the Boeing strike action that depressed aircraft-related investment. These factors will unwind this quarter, but the downside risk is surging imports as US companies seek to avoid potential tariffs that could kick in from this weekend

| 2.3% |

4Q 2024 GDP growth |

Strong consumer drives growth

US fourth quarter GDP grew at a 2.3% annualised rate, a little below the 2.6% consensus, but the details tell a more robust story that will keep the Fed wary about easing monetary policy too far too fast.

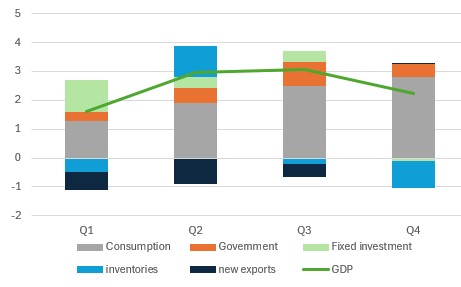

Household-related activity continues to drive the growth story with consumer spending expanding much more rapidly than expected at 4.2% annualised while residential investment jumped 5.3%. Net trade neither added nor subtracted to overall growth in the final three months of the year despite yesterday’s surprisingly large trade deficit figures for December. Meanwhile government spending increased 2.5%.

What prompted the weakness relative to expectations was primarily a big draw down of inventories that subtracted nearly a full percentage point from the headline growth rate. It may be that the surprise strength in consumer spending contributed here. Non-residential investment fell 2.2% – primarily due to a 7.8% drop in equipment, which we attribute to Boeing strikes.

Contributions to US annualised growth (%)

Gradual cooling anticipated for 2025

Consequently, the breakdown is better than the headline suggests with inventories likely to rebound next quarter and aircraft-related investment set to recover this quarter. However, net trade is probably going to be a big drag as companies look to bring forward imports to get ahead of potential tariffs while the stronger dollar will increasingly hurt export competitiveness. At least there is strong momentum in the consumer sector to provide a solid base for growth.

In terms of the outlook President Trump is looking to create a low taxation, light touch regulatory environment in order to boost growth prospects while implementing tariffs to improve US manufacturing competitiveness and promote re-shoring of economic activity. This should all be supportive for economic activity, but at the same time there is evidence of a cooling jobs market and nominal income growth is slowing notably – look for a further deceleration in tomorrow’s employment cost index.

Moreover, the Federal Reserve’s 100bp of rate cuts since have been counteracted by the 90bp rise in Treasury yields, which has translated into higher corporate borrowing costs and higher mortgage rates for home buyers. Credit card and consumer loan borrowing rates have barely responded while the dollar is up around 8% on September’s levels, which will also act as a headwind to growth. Consequently after 2.8% growth in 2024 we look for GDP growth closer to 2.3% in 2025.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more