Rising inflation complicates the CEE’s economic recovery

The CEE region’s economic recovery continues and we expect this to continue in the months ahead, although the data is mixed. Inflation has also picked up and is expected to head more to the upside in most of the region, complicating further monetary easing

Poland: Gradual GDP and inflation recovery

Data on this year's first quarter GDP (up by 2.0% year-on-year) and its composition confirmed that the Polish economy is on a path to recovery – albeit a one-legged recovery. Household consumption jumped by 4.6% YoY on the back of a buoyant increase in real disposable income fuelled by rising labour income (double-digit growth in wages) and a generous indexation of social spending (pensions, child benefits) amid lower inflation. Public consumption soared 10.9% YoY, boosted by increases in public sector wages.

At the same time, the 2023 investment came to a halt as fixed investment fell by 1.8% YoY after rising 15.8% YoY in the fourth quarter of 2023 and 13.1% in 2023 as a whole. It was significantly boosted by public investment in 2023 as the projects from the 2014-2020 EU financial framework were completed. The strong performance of public investment (5% of GDP in 2023) is unlikely to be repeated in 2024 as the new EU budget is starting slowly, and Recovery and Resilience Facility projects are significantly delayed. We still see 2024 GDP growth at 3% amid a rebound in consumption.

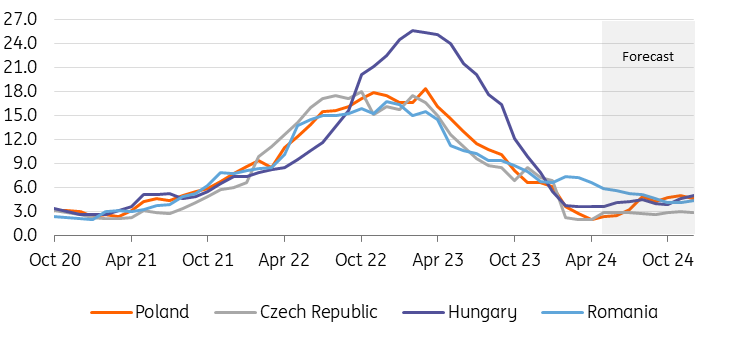

CPI inflation has started trending upwards, even as the flash reading for May surprised to the downside. With most of the energy shield to be scrapped in the second half of 2024, headline inflation is projected to continue trending upwards and reach around 5% YoY in December this year. At the same time, core inflation keeps running close to 4% and pressure on services prices from rising wages is still significant. In such an environment, the Monetary Policy Council is unlikely to start the monetary easing cycle this year, as quite clearly flagged by National Bank of Poland Governor Adam Glapiński in May. The first cuts are expected to take place in 2025 (potentially not earlier than in the second quarter) and be limited in scale.

Headline inflation (%YoY)

Czech Republic: Inflation to remain elevated amid strong consumption but weaker investment

The Czech economy is expected to see a continued cyclical recovery driven by an improving export side and upbeat domestic consumption. The renewed real wage growth of 4.8% YoY in the first quarter will support consumer spending as the emerging rebound of main eurozone trading partners fosters exports. A gradual economic rebound can also be seen in leading indicators such as lofty retail sales and overall positive consumer sentiment.

That said, the extraordinary plunge in fixed capital formation from the first quarter paints some fragility in the recovery for the medium term. Fixed investment plummeted 7.9% from the previous quarter, bringing investment levels back to numbers observed in 2018 and limiting the scope for a full-fledged recovery. This leads us to revise our growth forecast to 1.1% for this year, below the Czech National Bank (CNB) forecast. That said, the gross fixed capital formation represents a good candidate for an upward revision in the next GDP estimate at the end of this month. We assess the weakness in investment as a symptom of structural issues that prevent the country's full economic potential being reached this year and into the next.

PMIs remain in contractionary territory, signalling continued weakness in the Czech manufacturing sector. Still, an upward trend from the beginning of this year supports our take on a gradual way out of last year’s economic malaise. Overall input price inflation in industry has cooled down, while the reported pass-through to customers has remained strong. This shows that the medium-term price pressures are not quite at bay amid the return of consumer spending and improving foreign demand.

The upward inflation surprise at 2.9% in April, stronger household consumption and loftier nominal wage growth resulted in an upward revision of our inflation forecast to 2.5% for this year. Both nominal and real wage growth dynamics were 0.6 percentage points stronger than the CNB projection. Strong household spending, higher food prices, and still-elevated price growth in the service sector will contribute to more consciousness in the current CNB easing cycle. Still, monetary policy conditions are rather restrictive right now, so the easing will likely carry on though in a restrained mode. We foresee a 25bp cut at the June meeting, with the terminal rate at 4.50% this year and 3.75% for next year.

Hungary: Sensing some optimism

While we have not made a 180-degree turn in our outlook for Hungary, we acknowledge that there have been some positives recently. In general, the high-frequency data still paints a somewhat cloudy picture, but if the recent upturn in retail sales continues, we can clearly say that some rays of light are breaking through the clouds. However, it is not only retail spending that is clearly raising hopes that Hungary is indeed recovering. The labour market has shown resilience, with the employment rate rising and the number of unemployed falling in recent months.

The real surprise with the labour market is that wage growth is still hot. Although company surveys at the beginning of the year pointed to a marked slowdown in wages in 2024, the first quarter data contradicts the survey results. It may be that firms were expecting a looser labour market, while in reality, it has remained relatively tight, keeping employers in the "we have to pay them" camp. Disinflation ended in April and while we still expect two waves of reflation (May and October), we believe the first will be much weaker than expected. This is mainly due to falling fuel and food prices, which are keeping the overall monthly price increases in check. As a result, we lower our full-year inflation forecast by 0.3ppt to 4.25% in 2024.

The one segment of the economy that is still resisting the slow infiltration of optimism is the external balance. While both the trade in goods and current account surpluses have provided significant upside surprises, we believe they are for the wrong reasons. Import activity remains subdued on the back of still weak (albeit improving) domestic demand, while depressed industrial production is keeping energy demand in check. On the other hand, export activity is largely driven by the sale of stocks of grain and grain products, and once this effect wears off, manufacturing exports still won't be there. As a result, we continue to call for a deterioration in the external balance from here and a negative contribution from net exports to the expected 2.2% GDP growth in 2024.

On the market, the most notable story is the HUF sell-off at the end of May, which was a good illustration that the forint remains the most vulnerable currency in the CEE region. It also showed that the previous strengthening was a combination of global factors and tactical trading. Looking ahead, the forint remains exposed to political and fiscal risks as well as the ongoing cycle of interest rate cuts, in our view.

Romania: Consumption prospects remain solid while fiscal slippage persists

Private consumption is set to re-emerge as the key growth driver this year. Over the first quarter, retail sales grew by an impressive 5.0% versus the previous quarter, one of the strongest performances on record. With public wages and pension hikes already planned for this year, the momentum should remain strong. That said, the first quarter flash GDP did not impress. The second GDP reading on 7 June should bring additional clarity – if the numbers are reconfirmed, it would likely mean that delayed investments or weak net exports were a drag on output. We hold on to our 2.8% growth projection in 2024.

On the monetary policy front, we now think that the National Bank of Romania is preparing the groundwork for an August rate cut. Strictly on macro considerations, risks for rates are skewed to the upside as long as the strong consumer momentum, high wage growth and large fiscal slippages continue. On another note, it’s worth mentioning that the political arena is also currently discussing the composition of the new National Bank of Romania board, which is set to be sworn in by the end of June. All in all, we expect a cautious and gradual easing cycle ahead, with only 50bp of cuts by the year-end, taking the key rate to 6.50%.

On the fiscal front, the budget deficit slipped visibly to 3.24% of GDP in January-April (2024 official target: 5.0% of GDP). At this stage, we push up our 2024 deficit forecast from 6.0% to 6.5% of GDP, with upside risks still at play. The key factors to watch ahead are the outcome of the negotiations with the European Commission (EC) in June and how well officials will play the “Romania needs investments” card. Getting to -3.0% of GDP seems a matter for the next electoral cycle after 2028.

Download

Download article

7 June 2024

ING Monthly: All eyes on Europe This bundle contains 13 articles

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more