Rates Spark: The Fed will not do nothing

Wednesday features the Fed – we watch for any messaging on liquidity management. Any spillovers from the Fed meeting to the eurozone may be muted as especially the front end of the swap curve has shown little correlation with US rates recently. The back end remains more sensitive to US dynamics and thus we maintain a steepening bias from a structural perspective

Some focus on reserve management is possible from this “no change” meeting

The minutes from the December meeting noted that usage of the overnight reverse repo facility remained on a declining trend, reflecting money market fund reallocation to Treasury bills and private-market repo, which offered slightly more attractive market rates. This occurred against a tightening in market repo conditions, and continued increases in net Treasury bill issuance. At that meeting, the Fed also reduced the rate it pays at the reverse repo window by 5bp, back to flat to the funds rate floor. This adds to the attraction of market repo, and should correlate with further falls in the use of the reverse repo window. Our view is that usage of the reverse repo window will ultimately fall towards zero, barring some temporary spikes around month end.

The Fed may or may not comment on the above. It will also be interesting to see whether the Fed comments on the resurrection of the debt ceiling since 2 January 2025. While it’s too early to expect a material market focus on it, the technical aspects of it are impactful. As long as the debt ceiling remains in place and the Treasury employs extraordinary measures to avoid breaching it, there is a tendency to spend down the cash balances that it holds at the Fed. As these get spent down, they add to reserves in the system which in turn acts to counter the tightening effect of the ongoing quantitative tightening (QT) programme. In effect, hitting the debt ceiling forces the Treasury to be a net supplier of liquidity to the system.

Despite these complications, the Fed may well lay the groundwork for ending QT at some point in 2025. This is the case as excess liquidity (which we define as bank reserves plus reverse repo balances) is likely to hit levels that the Fed would prefer not to go below from the middle of 2025 onwards, partly depending on how the debt ceiling saga evolves. The key number here is US$3tn for reserves, representing about 10% of GDP. We are currently at US$3.5tn. So we’re comfortable. At the same time, the reverse repo balance is running at US$100bn, and if that were to hit zero, then we’d hit some degree of tightness. That’s close, as QT is running at US$60bn per month. QT may have to end by mid-2025 based on a simple extrapolation of this.

Short end of euro swap curve is disentangling from US rates

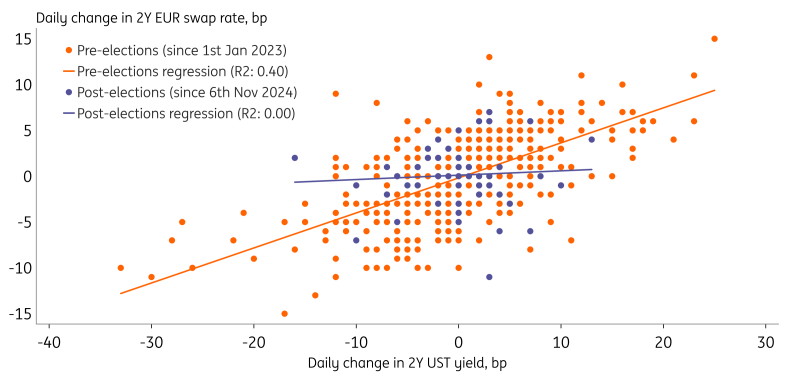

Since Trump’s election in November 2024, the front end of the euro swaps curve has started to move more independently from US rates. Before the elections, around 40% of the daily variance of the EUR 2Y swap rate could be explained by 2Y UST yields. Yet as seen in the chart below, that correlation has since reduced to zero. Part of this reduction can be explained by the opposing effects US tariffs would have on inflation. Therefore tariff threats helped rates move in opposite directions. But also the macro data and the economic outlook have become more disentangled, leading to separations of the expected policy paths.

The increased independence of the front end of the curve suggests that the European Central Bank can exert more influence over the rates market through forward guidance. Thursday’s meeting could therefore bring about a material rate reaction if the ECB decides to emphasise concerns about growth. Vice versa, the upcoming Fed meeting may not have much of a lasting impact on EUR rates. The back end of the curve remains sensitive to the US, however, so any moves in the 10Y UST yield would find itself spill over to the eurozone. Therefore we reassert our view that the euro swap curve has more steepening potential.

Correlation between 2Y UST and EUR swaps turned zero

Wednesday’s events and market view

The FOMC meeting takes centre stage on Wednesday with only few notable events ahead of it. In the eurozone we will get the German consumer confidence reading and later the ECB’s M3 data. Bank of England Governor Bailey will speak at a Treasury Committee hearing on November’s Financial Stability Report.

In primary markets Germany is auctioning €4.5bn of 10Y Bunds while the UK sells £3bn 9Y green gilts.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more