Our July guide to global central banks

Everything you need to know about central bank policy around the world over the coming months

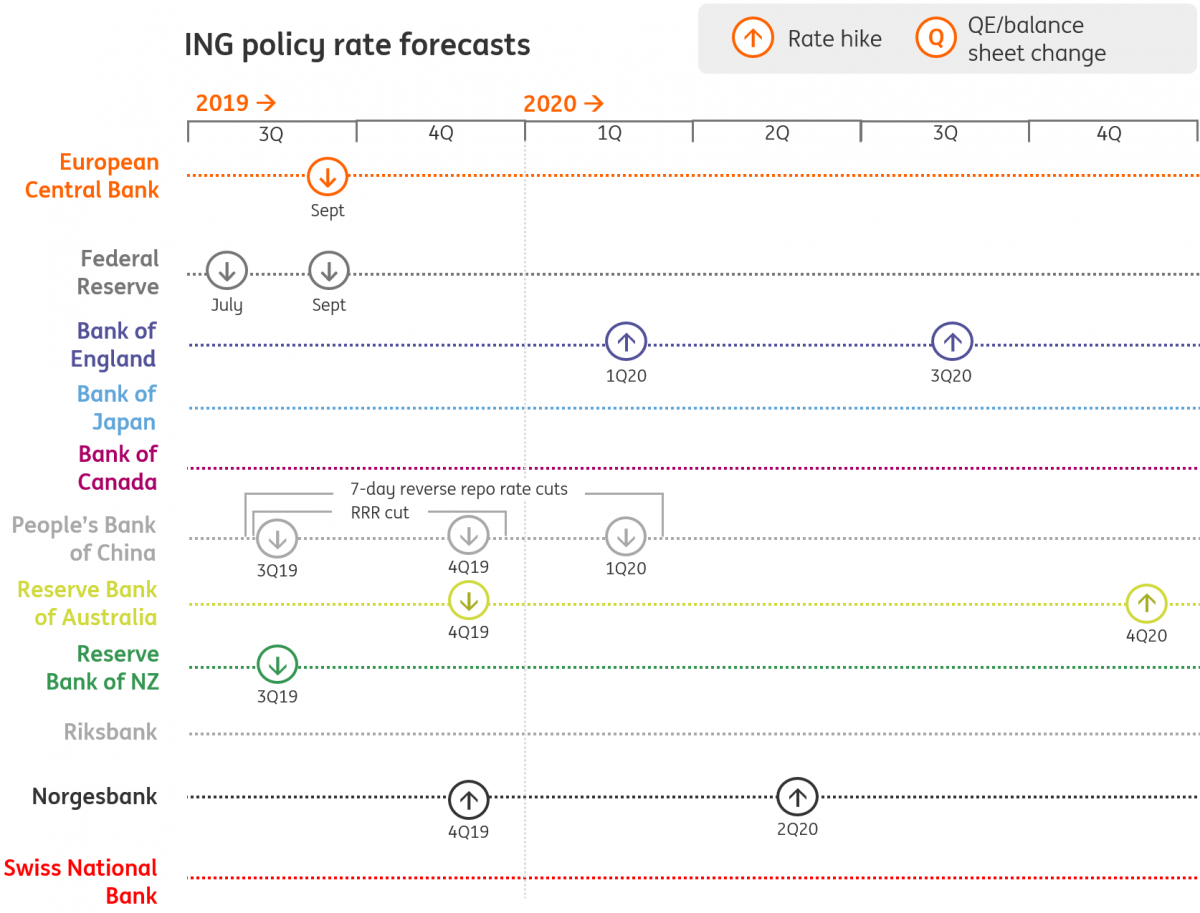

Our central bank outlook

Federal Reserve: Prevention versus cure

A ceasefire has been called in the US-China trade war, but we doubt the truce will hold for long given the two sides remain a long way apart on key issues such as technological transfers, intellectual property rights and the trade dispute resolution mechanism.

A new round of tariff hikes will contribute to more pronounced economic weakness by disrupting supply chains, putting up costs and hurting profit margins. Such an environment would be negative for equity markets and make US businesses more reluctant to invest and hire new workers.

Given the expectations of renewed trade tensions, we look for an early precautionary 25bp rate cut in July, followed up with another 25bp move in September

At the June FOMC meeting, the central bank talked of increased “uncertainties” about the economic outlook which they will “closely monitor”. Federal Reserve Chair Jerome Powell subsequently repeated his comment “an ounce of prevention is worth more than a pound of cure”. Given the expectations of renewed trade tensions we, therefore, look for an early, precautionary 25bp rate cut in July, followed by another 25bp move in September.

A 50bp July rate cut had been seen as a possibility at one point, but given St Louis Fed President James Bullard, who was the only Fed officials to have voted for a June rate cut, suggested such aggressive action “would be overdone”, this looks unlikely. Nonetheless, the market is pricing in three rate cuts in total this year with a further 25bp cut in early 2020.

We don’t expect such aggressive action given our belief that President Trump wants to win re-election and will, therefore, be prepared to sign a trade deal, probably in 4Q, that doesn’t necessarily meet all of his initial demands. A rising equity market and healthy economy gives him the best chance to succeed.

The Federal Reserve is covered by James Knightley

We think the market is overestimating Fed rate cuts

European Central Bank: Leaving with a bang

ECB president, Mario Draghi’s Sintra speech has made clear that the question regarding the short-term outlook for the ECB is no longer “what negative surprise is needed for the ECB to cut rates” but rather “what positive surprise could actually prevent the ECB from cutting rates”. Predicting the exact timing is more complicated though. In fact, traditional ECB watchers argue in favour of compiling more data, waiting for the release of Q2 GDP in mid-August and the next ECB staff projections and then take a decision at the September meeting. Draghi’s track record in overdelivering and trying to be ahead of the curve, however, could bring a rate cut already at the ECB’s July meeting.

We think the ECB will want to wait until the September meeting to deliver a 10bp rate cut in the deposit facility

It’s a close call but unless the days leading up to the July meeting bring more disappointing macro data, we think the ECB will want to wait until the September meeting to deliver a 10bp rate cut in the deposit facility, combined with a clear commitment to restart QE, or if need be even actually start QE. The reason not to use all ammunition at once would be to have some policy measures left in case of a disorderly Brexit. However, chances are increasing that Draghi will leave office with a bang.

The ECB is covered by Carsten Brzeski

Eurozone sentiment has deteriorated

Bank of England: Caution creeps in as ‘no deal’ Brexit fears resurface

Markets are now pricing close to a 50% probability of a rate cut by the end of 2019. At the same time, Bank of England policymakers have hinted that rates could move higher again depending on how Brexit pans out. So who's right?

A rate hike later this year shouldn't be ruled out completely, although, given all the noise on Brexit, we think it is unlikely

Well, for the time being, the economic outlook warrants caution. While the slowdown in second-quarter growth was exaggerated by a fall in production, the underlying momentum remains weak. Consumer spending, for instance, had a fairly bad quarter despite some modest recent improvements in real incomes. We also expect business investment to resume its decline over the summer months, as Brexit uncertainty picks up and the perceived risk of a general election later in 2019 increases.

That said, policymakers are heavily focussed on wage growth, which has been performing solidly over the past year-or-so and this was key to its rate hike rationale in 2017/18. Assuming this trend continues, a rate hike later this year shouldn't be ruled out completely, although, given all the noise on Brexit, we think it is unlikely.

The Bank of England is covered by James Smith

Our latest Brexit scenarios

Bank of Japan: Are there any tools left?

There is almost nothing new that can be said in relation to the Bank of Japan. Each month, Governor Haruhiko Kuroda’s press briefing outlines measures he claims could be utilised to help the quest for target inflation, a quest that doesn’t go anywhere. Markets ignore it. Recently, however, despite the usual tired assurances, we have noticed the money stock beginning to rise again after almost a year where it peaked.

With no credible tools at their disposal, we suspect any policy changes by the BoJ will wait until they have absolutely no other option but to act

This has coincided with lower 10-year Japanese government bond (JGB) yields, though rather than attribute any causality to these movements, we think the JGB yield decline is just a reflection of low US Treasury yields, though just possibly there is some overlap between these events.

With no credible tools at their disposal, we suspect any policy changes by the BoJ will wait until they have absolutely no other option but to act. For this, we suspect we will need to see USD/JPY at 100 and threatened on the downside, at which point, lower bond yield targets and possibly more negative rates could be employed. Increased asset purchases aren’t feasible with supply limited, so any announced increase would simply not happen.

If we ever get to this point, we doubt these measures would be successful. A short term reversal at best.

The Bank of Japan is covered by Rob Carnell

Japanese vs. US yields

People's Bank of China: Boosting liquidity to support stimulus

The headwinds from the trade and technology wars have inevitably affected the Chinese economy.

In the past, we have argued that the central bank may be reluctant to use the reserve requirement ratio (RRR) for major easing, given that it is one of the more rigid liquidity management tools. Once cut, the liquidity injection is long-lasting.

We expect the central bank to inject even more liquidity into the system, either via RRR cuts or the medium-term lending facility

But it has been reported that the People's Bank of China is now not only considering cutting the RRR to provide liquidity, but also cutting interest rates, and this is linked to the recent fiscal stimulus. Increased infrastructure spending created demand for money, which could easily push up interest rates – something that isn’t the policy’s intention.

As a result, the central bank must provide liquidity big enough to suppress this upward pressure on Chinese interest rates. The PBoC has already pumped around CNY 550 billion in May and CNY107 billion in June, which saw the overnight SHIBOR edge to 0.877% on 3 July, not far off the previous low of 0.80% in March 2009.

As the economy needs more stimulus, we expect the central bank to inject even more liquidity into the system, either via RRR cuts or the medium-term lending facility (MLF). Both can be done in a targeted or broad-based manner depending on how much liquidity the economy needs.

The People's Bank of China is covered by Iris Pang

SHIBOR has edged lower following the central bank's actions

Swiss National Bank: We don't expect lower rates in the near-future

The Swiss central bank kept its monetary policy unchanged in June, leaving the main rate at -0.75% - the lowest policy rate in the world. It has also reiterated its willingness to intervene in the foreign exchange market if it proves necessary. Unlike some other major central banks, the SNB hasn't really hinted at an easing bias at this meeting. That said, this does not mean the SNB is in the process of normalising its monetary policy - on the contrary, we believe the key rate will not increase for years.

We believe the first thing the SNB will do when the Fed and the ECB cut rates is to intervene if necessary in the foreign exchange market to offset any appreciation in the Swiss franc

On the other hand, we believe the SNB does not intend to lower its, already very low, rate in the near future. We believe the first thing the SNB will do when the Fed and the ECB cut their rates is to intervene if necessary in the foreign exchange market to offset any appreciation in the Swiss franc. If that's not enough and we were to see a big effect on the EUR/CHF exchange rate, the SNB may then consider loosening monetary policy further by cutting its policy rate.

After all, members of the SNB’s governing board have said many times that there is still some room to cut rates further. In that case, it could increase the exemption threshold from the negative interest applied to sight deposits to lower the burden on banks. However, this would not solve the side effects linked to negative interest rates on the mortgage sector (bubble risk) and that's why we think they'll first try to avoid a rate cut.

The Swiss National Bank is covered by Charlotte de Montpellier

Swiss inflation rates

Riksbank: Resisting the ECB's dovish lure

In times gone by, fresh ECB stimulus may well have been mirrored by Swedish policymakers, keen to limit the spillover to the krona. This time, things look a little different. With EUR/SEK above 10.50, the Riksbank appears more relaxed about potential currency strength. If anything, our FX team thinks the krona could weaken further as concerns surrounding global growth outweigh the impact of the dovish ECB (which is largely priced in).

We don't expect the Riksbank to ease policy, although equally, we think the central bank is unlikely to follow through with its forecasted rate hikes for later this year or early 2020

We, therefore, don't expect the Riksbank to ease policy, although equally, we think the central bank is unlikely to follow through with its forecasted rate hikes for later this year or early 2020. Domestic demand is lacklustre, as the lagged effect of earlier property price declines continues to weigh on construction and consumer activity. There are also some early signs that inflation expectations are slipping among labour organisations - another indication perhaps that the 2020 wage negotiations may not yield the kind of uplift in pay growth the Riksbank is currently forecasting.

Trade tensions could also spell bad news for Sweden's relatively open economy - in the context of possible US auto tariffs, car exports make up 7.5% of the total, and the US is the biggest customer.

The Riksbank is covered by James Smith

Riksbank relaxed about possible SEK strength following the ECB

Norges Bank: The hawkish outlier

In stark contrast to many of its developed market peers, Norges Bank took its tightening cycle a step further last month by increasing interest rates for the second time this year. What’s more, the central bank expects it will “most likely” hike rates again later in 2019, and this comes as the energy sector continues to drive growth higher.

We expect the next rate hike in December, although we wouldn’t fully rule out an earlier move at the September meeting

While oil prices have slipped off their April highs, the breakeven cost of production in Norway stands significantly below current market pricing according to Norges Bank. This is incentivising firms to invest, and the latest oil investment survey indicates that firms will spend even more in 2019 than previously anticipated.

We expect the next rate hike in December, although we wouldn’t fully rule out an earlier move at the September meeting.

Norges Bank is covered by James Smith

Norwegian firms have recently increased their estimates for 2019 oil investment

Bank of Canada: Cautious optimism

Canada’s temporary soft patch appears to be coming to an end with 2Q indicators suggesting a reasonable bounce-back in growth. Business sentiment has recovered while rising oil prices are clearly supportive of activity in the energy sector. Unemployment has hit a new all-time low of 5.4% and wages are responding, which is boosting consumer sentiment and spending.

We expect the BoC to keep the overnight rate unchanged at 1.75% throughout the next 18 months

There have also been positive developments on trade with the removal of steel and aluminium tariffs while the US-Mexico-Canada trade agreement is in the process of being ratified. However, the lingering US-China trade tensions remain a threat and any re-escalation could make the Bank of Canada more cautious on the economic outlook.

For now, the economic backdrop is reasonably robust while inflation has recently surprised on the upside on all key measures. We also have to remember that the Bank of Canada didn’t hike interest rates as aggressively as the Federal Reserve, hence why BoC officials continue to talk of monetary policy “accommodation”. While the Fed stands ready to offer support to the US economy, there appears less need for Canada to do so.

Given our assumption that the US and China agree a trade deal later this year we expect the BoC to keep the overnight rate unchanged at 1.75% throughout the next 18 months.

The Bank of Canada is covered by James Knightley

Bank of Canada and US Federal Reserve interest rates

Reserve Bank of Australia: Expect another cut in the fourth quarter

The Reserve Bank of Australia cut rates for the second consecutive month in July, taking the cash rate target to 1.0%. But although it is highly doubtful that 50bp will be enough to bring the unemployment rate down to the levels the RBA believes will be necessary to drive up wages and inflation (4.5% from today’s 5.2% rate), Governor Philip Lowe was keen to quell expectations of even more to come, with the key phrase of his briefing later that day “…we will be closely monitoring how things evolve over the coming months. Given the circumstances, the Board is prepared to adjust interest rates again if needed to get us closer to full employment and achieve the inflation target”.

We now see rates troughing at 0.75% after one more rate cut in 4Q19

What this seems to suggest is that the RBA is not going to rush the next cut and we may have quite a pause for them to digest how the first cuts are working out. We thought the RBA might take more time with their earlier cuts, so are a bit surprised at this approach, but it can be rationalised as trying to get the most out of what is a very limited supply of ammunition of questionable effectiveness.

Markets, which had been undertaking a sort of US-style aggressive pricing of easing were already scaling back on this in the aftermath of the G20 meeting and have gone further since. We now see rates troughing at 0.75% after one more rate cut in 4Q19, though this is dependent on some slightly stronger price and activity data, though we don’t hold out any realistic hopes for the RBA to hit their inflation target anytime soon.

The Reserve Bank of Australia is covered by Rob Carnell

Australian policy rate expectations

Reserve Bank of New Zealand: August rate cut looks likely

In contrast to the Reserve Bank of Australia, where rate cuts have been met by a market paring back expectations for more, the market implied rate for Reserve Bank of New Zealand policy rates have changed little since the G20 meeting. With a meeting on 7 August, we think there is a very good chance of another rate cut, after the pause at the 26 June meeting.

With a meeting on 7 August, we think there is a very good chance of another rate cut, after the pause at the 26 June meeting

New Zealand’s newsflow has not been at all supportive of a further pause in rates, and the wait-and-see stance that they took in contrast to the more proactive RBA approach, is now being tested, as signs that growth is slowing further emerge business confidence slumps, and house price growth slows further.

Markets are implying rates fall a further 25bp before troughing. But with no recovery expected by end-2021, the risk has to be that this moves to price in further easing as the RBNZ satisfies immediate market requirements for more easing. Here, a more front-loaded approach might have achieved more.

The Reserve Bank of New Zealand is covered by Rob Carnell

New Zealand policy rate expectations

Tags

Central BankDownload

Download article

9 July 2019

What’s happening in Australia and the rest of the world? This bundle contains 7 articlesAuthors

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more