OPEC+ kicking the can down the road

A handful of OPEC+ members decided to extend supply cuts into next year and also slow the pace at which they will bring supply back onto the market. While this move reduces the scale of the surplus expected next year, the market is still set to see a surplus in 2025. The extension in cuts has led us to make small revisions higher to our forecasts

OPEC+ extends additional voluntary supply cuts

OPEC+ members decided yesterday to extend their additional voluntary supply cuts of 2.2m b/d by a further three months, which means the group is now currently set to gradually increase supply from only April 2025.

In addition to a further delay in bringing supply back, members will also bring this supply back at a slower pace. Previously, the group were set to bring 2.2m b/d of supply back online over the course of 12 months. However, members will now bring this supply back over the course of 18 months. So, this full supply is scheduled to return by September 2026.

The market seemed somewhat disappointed or at least indifferent to the extension with ICE Brent settling 0.3% lower on the day, leaving it just above US$72/bbl. This suggests that the market was expecting a more aggressive move from OPEC+.

How does this change the oil balance for 2025?

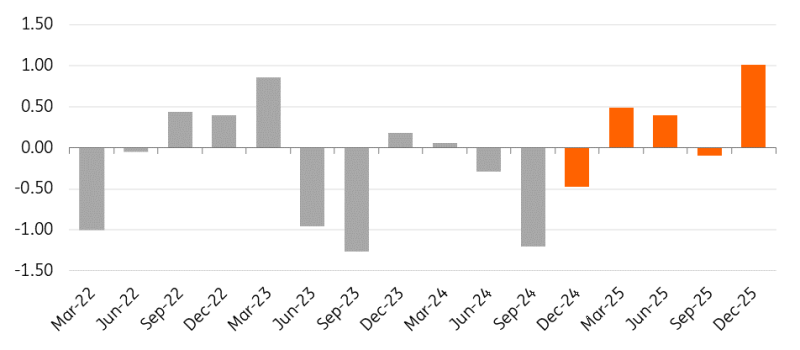

The action taken by OPEC+ eats quite heavily into the surplus that was expected over 2025. However, the extension and the slower return of barrels is not enough to push the market into deficit next year. The move still leaves the market in surplus in 1H25, although admittedly the surplus is more manageable at around 500k b/d, compared to 1m b/d expected previously.

For the peak demand period of 3Q25 we now see the market essentially in balance, before returning to a surplus of 1m b/d in the final quarter of 2025.

While the action taken by OPEC+ may potentially provide a higher floor to the market than previously expected, ultimately the group will still have to accept lower prices. OPEC+ faces the ongoing issue of growing non-OPEC supply and disappointing demand growth, largely due to China. Expectations for global demand growth going into next year remain modest at less than 1m b/d. While part of this demand slowdown is cyclical, there is also a large part which is structural, due to the higher penetration rates of new energy vehicles.

Global oil market to remain in surplus in 2025 (m b/d)

What does it mean for our price forecasts?

Expectations for a smaller surplus means that downside for ICE Brent is likely more limited in 2025 than initially expected. Previously, we had forecast ICE Brent to average $69/bbl over 2025. However, following this action from OPEC+ we have increased this to $71/bbl. The fact that the market will still be in surplus means that there is still downside in prices from current levels, particularly in 4Q25. Risks to this view include OPEC+ extending these cuts even further into 2025 and stricter enforcement of oil sanctions against Iran.

Download

Download articleThis publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more