Increase in minimum reserves would hit bank liquidity at crucial moment

The European Central Bank is said to be considering an increase in banks' minimum reserve requirements. The impact of higher reserve requirements on banking sector profitability would be negative. This would also tie up a larger share of bank liquidity buffers and therefore have a substantially negative impact on LCR metrics

ECB looks for ways to curb excess liquidity

Among potential ways to reduce the excess liquidity in the banking system, the ECB is reportedly considering increasing the minimum reserve requirements (MRR). Several ECB policymakers are said to be in favour of a move higher in MRRs to 3% or even to 4%. Both the Belgian central bank’s Pierre Wunch and the ECB’s Pablo Hernández de Cos have indicated they do not see “strong arguments” for this, or see this as “obvious” while the Bundesbank’s Joachim Nagel has indicated he would support a move higher.

Currently, banks have to meet a 1% minimum reserve requirement on average during the reserve maintenance period.

The 1% MRR corresponds to €165bn for the sector. If the ECB were to increase the MRR to say 3%, the MRR would increase by €330bn to close to €500bn. Setting the requirement to 4% would result in an increase of €500bn to €660bn assuming other things stay intact.

A higher MRR would have several negative implications for the banking system.

Dent on bank profitability

Higher required minimum reserves would, other things being equal, reduce the amount of funds that banks can deposit at the ECB's deposit facility. As the ECB pays interest on the deposit facility but not on the minimum reserves, higher required reserves would represent a drag on net interest income.

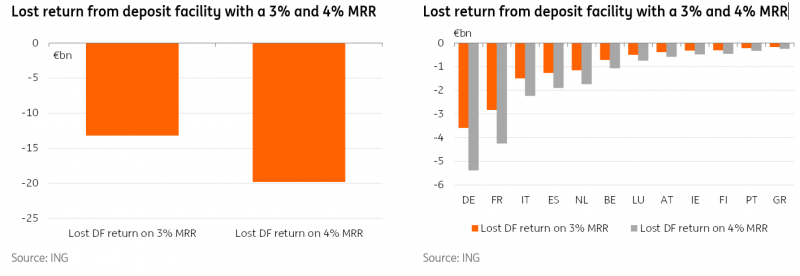

We calculate that raising the minimum reserve requirement from 1% to 3% or even 4% would cost €13bn-€20bn in lost interest on the deposit facility for the eurozone banking system based on the current deposit facility rate.

The largest absolute impact would be felt by German banks, followed by French, Italian and Spanish names. Taking into account the relative size of the banking sector (total MFI assets), the impact would be largest for banks in smaller countries, however, such as in the Baltics, Cyprus and Slovenia, with Belgium also among the more impacted countries on a relative basis. The relative costs would be more limited for banks in Ireland, France and Germany when considering the MFI balance sheet size.

Increase in MRR would result in smaller revenues for banks from the ECB deposit facility

But the larger unknown comes from the actual liquidity drain

The increase in minimum reserve requirements would also have a negative impact on banks' liquidity positions. Banks have to meet a 100% Liquidity Coverage Ratio (LCR) requirement. For the LCR calculation, banks can include in their Level 1 assets reserves at the central bank provided that the credit institution is permitted to withdraw such reserves at any time during stress periods (see Article 10(1) (b) (iii) of the Commission Delegated Regulation (EU) 2015/61). More specifically, based on the ECB guidance from 2015, the part of the daily account holdings that exceed the average daily required reserves is considered withdrawable at any time in times of stress and is eligible for inclusion in Level 1 assets. As such, central bank minimum reserves are not usable towards the LCR Level 1 liquidity buffers, meaning that increasing the requirements would have a similar negative impact on bank liquidity buffers.

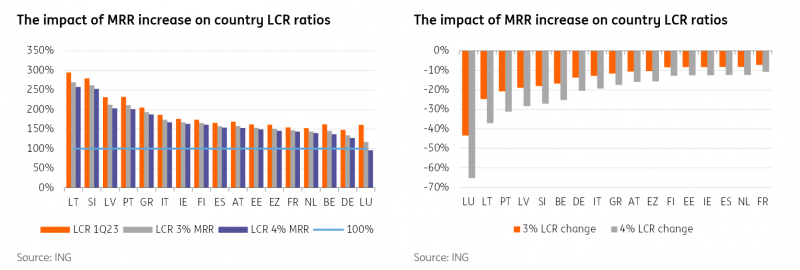

As of the first quarter 2023, the 111 significant institutions supervised by the ECB had an average LCR ratio of 161.3%. Of the total €5.1tn in liquid assets that these banks held, €4.9tn were Level 1 assets, with a limited amount of €149bn in Extremely High Quality Covered Bonds.

If the €5.1tn liquidity buffers of significant institutions were to absorb the MRR increase to 3% or 4%, the buffers would drop to €4.8tn or €4.6tn. This would roughly equate to a decline in the LCR of 10-16 percentage points. It is good to note that here, the actual impact would likely be smaller than this, as we have included liquidity buffers of only the larger banks (significant institutions) in our assessment.

On a country basis, while the potential decline in LCR would be larger for smaller banking systems on a relative basis, the impact for countries such as Germany and Belgium also looks hefty.

An increase in minimum reserve requirements would substantially pressure bank liquidity coverage ratios

And then what?

Banks would likely seek to take measures to offset part of the impact on profitability and liquidity metrics following an increase in the MRR.

One way would be to try and limit the size of the increase. The MRR is calculated based on shorter than two-year customer deposits and funding. Banks could seek to replace their shorter-term funding with longer-term funding. They could also try and rebalance their funding profile away from deposits towards bond markets. This would limit the increase in deposit rates while the higher wholesale funding share would have a negative impact on net interest income. Not all banks can issue longer-term funding at sustainable levels, however. Even better-rated banks seem to have avoided printing at the longer end of the bank bond curve recently as investor demand seems to be mainly present at the shorter end and perhaps the belly of the curve due to the current interest rate expectations and the shape of the curve.

The potential negative impact on liquidity buffers is large and would come in an environment with recent bank failures both in the US and in Switzerland that were all in one way or another driven by a sudden loss of liquidity. We consider a decline in liquidity buffers as a risk factor, in particular in the context of the ongoing decrease in the TLTRO-III funding programme with the total programme maturing in 2024.

Some very liquid banks could absorb the drain in their LCR ratios with existing buffers. Others would likely try and replenish the levels. Alongside lowering the MRR, alternatives here would include cutting back lending or perhaps increasing wholesale funding to replenish liquidity buffers.

Banks most hit by the change would be those with lower credit ratings, as they would have to pay more in the form of higher risk premiums for their bond market funding. In the end, more banks could end up using the normal ECB funding operations which, in the past, have been associated with a negative stigma and offer only a short-term relief due to the relatively short maturity of three months in the case of LTROs.

An increase in minimum required reserves would be clearly negative for banks. While the excess liquidity of €3.66tn still sloshing around in the system would limit the impact to some extent, in combination with the expected run-off of the TLTROs, we believe there could be a risk of unintended consequences.

If the ECB wanted to limit the likely bank liquidity impact, it could look into adjusting the LCR calculation in relation to minimum reserves.

Download

Download articleThis publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more