Global central banks in 2021

Global central banks have had a busy 2020, but their job is far from over. What tools do policymakers have left to deploy and what should we expect from monetary policy in 2021?

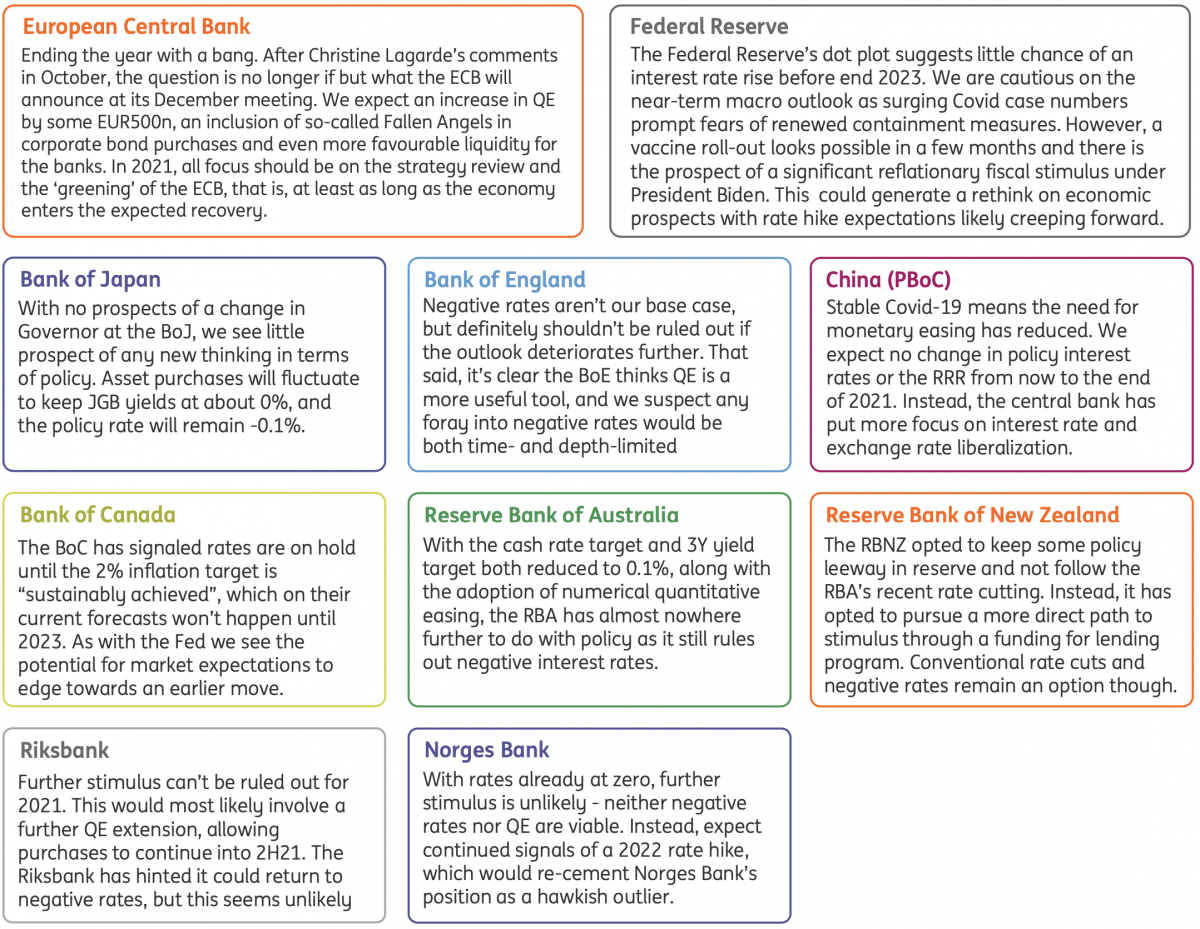

The outlook for central banks in 2021

Federal Reserve

Financial markets have performed strongly since it became clear that Joe Biden will be the next President of the United States while positive newsflow on a Covid-19 vaccine has provided further fuel for the rally in risk assets. However, we are becoming more concerned about the near-term story with unemployment benefit income being tapered for millions of households at a time when Covid-19 cases are rising rapidly. Vaccines could take several more months to roll out so we have to acknowledge the possibility for the return of pandemic containment measures in the US, similar to what Europe is currently experiencing, in an effort to limit the strains on the healthcare sector.

We remain very upbeat on the prospects for 2021 and 2022, which could help pull interest rate hike expectations forward from 2024

Legal challenges surrounding the election could intensify already high levels of political animosity, which may hamper the ability or limit the desire for politicians to agree to a swift package of measures that could support the economy during this period. This could make the Federal Reserve feel compelled to step up via asset purchases and/or liquidity injections to calm nerves and ensure smooth market functioning if we are correct and the economy enters a more troubled period.

Nonetheless, there is scope for a significant fiscal package in excess of $1trn next year (equivalent to around 5% of GDP). This stimulus, when combined with a long-anticipated Covid-19 vaccine, can really lift the economy and drive growth. We consequently remain very upbeat on the prospects for 2021 and 2022, which could help pull interest rate hike expectations forward from the 2024 dateline currently implied by the Fed dot-pot.

Depending on how robust the recovery is, we could see Fed asset purchases slow or even stop during 2021.

European Central Bank

After Christine Lagarde’s comments at the October meeting, the only question is not if but what the ECB will announce at its December meeting.

Even recent news on a vaccine will not prevent a downward revision of the ECB’s growth and inflation outlook. As a consequence, we expect the ECB to announce an increase in its quantitative easing programme by around €500bn, the inclusion of the so-called 'fallen angels' into corporate bonds purchases and even more favourable liquidity for banks.

In our view, the ECB will want to keep maximum flexibility and therefore change its definition of price stability from ‘below, but close to, 2%’ to ‘around 2%’.

With the economy, hopefully, entering a sustainable recovery in 2021, the ECB’s focus will be on the strategy review. We expect the ECB to follow the Fed in putting more emphasis on the symmetry of its inflation target, without going all the way towards an average inflation target.

In our view, the ECB will want to keep maximum flexibility and will therefore change its definition of price stability from ‘below, but close to, 2%’ to ‘around 2%’.

Bank of England

The Bank of England has extended its quantitative easing programme to allow it to continue asset purchases throughout 2021, but the combination of the new UK-EU trading relationship and the risks surrounding Covid-19 suggest more stimulus may be needed. But will this involve negative rates? We think the jury is still out.

We think the BoE will steer away from negative rates, barring a significant deterioration in the outlook

Policymakers are currently collecting evidence from banks on the impact sub-zero rates may have on profitability, although we doubt this will ultimately be enough to block the policy. The central bank has already hinted it may follow the ECB’s lead with a tiered system of implementing negative rates.

Instead, the decision will hinge on MPC consensus on whether the policy would be of much use - and so far that’s not been the case. Our own feeling is that lower rates are unlikely to add a great deal of impetus to the recovery. We, therefore, think the BoE will steer away from negative rates, barring a significant deterioration in the outlook.

Instead, QE is likely to remain the tool of choice.

Bank of Japan

It has been many years since we have pretended that the Bank of Japan had anything relevant or interesting still to come in terms of monetary policy, and that remains the case.

Policy rates are at -0.1% and are unlikely to be cut again, and certainly aren’t going up for years to come. Likewise, we don’t see any merit in the central bank pushing bond yields substantially below zero – the current target. Indeed, their most recent policy push seems more concerned with shoring up the banking sector, something that has arguably been talked about, though not necessarily undertaken on a large scale, since the 1990s when the controversial “Convoy system” was implemented.

It has been many years since we have pretended that the Bank of Japan had anything interesting to come in terms of monetary policy

Returning to this theme won’t necessarily bring an end to Japan’s slow growth, low inflation or sluggish lending. But if turning deposits into profitable assets remains next to impossible in Japan, cutting fixed costs and overheads through mergers and acquisitions still seems a worthwhile endeavour, even if only to deliver a bit more support and stability to the banking sector.

People's Bank of China

The People's Bank of China has stopped cutting the loan prime rate since May 2020 and hasn't slashed the reserve requirement ratio since February.

Economic recovery from fewer Covid-19 cases has been the main reason behind the neutral stance. We expect no change in monetary policy until the end of 2021, instead the core focus of the central bank will be interest rate and exchange rate liberalisation.

We have seen more advocacy from the central bank governor urging banks to apply the policy rate and link it to pricing financial products. The central bank has also started to phase out the use of counter-cyclical factors in the USD/CNY daily fixing formula, which means the exchange rate is likely to be increasingly driven by the market.

Bank of Canada

The Bank of Canada, like the Federal Reserve, has effectively signalled a shift to average inflation targeting.

We don’t envisage any major changes to the central bank's policy mix in 2021 although market interest rate hike expectations could start inching up earlier

Their forward guidance now states that policy won’t be normalised until the 2% inflation target is “sustainably achieved”, which under their current forecasts is not expected to happen until 2023.

The central bank has also recalibrated its asset purchases so they are focused at the long end of the curve in the hope that a flatter, lower yield curve will deliver the conditions that give the most benefit to households and corporates. We don’t envisage any major changes to this policy mix in 2021 although as with the Fed, market interest rate hike expectations could start inching up earlier.

Reserve Bank of New Zealand

At its last meeting (10 Nov) the RBNZ left open the possibility of a single further conventional rate cut. In leaving cash rates at 0.25% at its latest meeting, the RBNZ noted “better than expected” economic activity. But at the same time, they kept their options open in terms of further easing of policy rates, including, controversially, negative rates.

In the meantime, the RBNZ, which already owns about 37% of the outstanding stock of government debt after only six months, is supplementing its QE programme with a NZD100bn funding-for-lending scheme. Against the backdrop of a red-hot housing market, even if the labour market remains soft, further rate cuts by any channel may prove awkward. And in all likelihood, the RBNZ is out of substantive further easing measures. In our view, all of this discussion about alternative policies is simply part of an elaborate attempt to manipulate market expectations. But even if we are right and there is no further easing, we don’t anticipate any tightening in 2021.

Reserve Bank of Australia

At its most recent rate meeting, the Reserve Bank of Australia cut the official cash rate and 3-year yield target to just 0.1% from 0.25% and implemented a (numerical) quantitative easing policy (yield curve control is already a form of QE). This new scheme was for bonds at a 5-10Y tenor.

With the Australian economy picking up after its lockdowns came to an end, it is not entirely clear why the central bank decided the economy needed this extra, and arguably very marginal, additional easing. The latest policy announcements had a very limited and temporary effect on both the Australian dollar and Australian bond yields.

Unlike the RBNZ, the Australian central bank Governor Philip Lowe remains unequivocal in his opposition to negative rates. So even more than the RBNZ, the RBA looks to have hit rock bottom for cash rates, and in all probability, for all other substantive incremental easing measures, though that may not stop them from implementing some additional “cosmetic” measures during 2021.

Riksbank

While Sweden continues to take a more liberal approach to Covid-19 restrictions relative to its European neighbours, the virus nevertheless poses risks for the domestic economy.

The first wave of the pandemic showed us that individuals are likely to ‘act with their feet’ by taking a more cautious approach to going out and about. That said, there are potentially some brighter spots, too. Manufacturing looks set to be less affected by lockdowns globally than in the first half of 2020 - good news for Sweden’s production-heavy economy.

More stimulus can’t be ruled out, but we’d continue to expect this to take the form of quantitative easing over a return to negative rates. The Riksbank currently plans to complete its balance sheet expansion by the middle of 2021, something that could be feasibly extended. But having hiked the repo rate out of negative territory at the end of 2019, and opting against returning below zero during the peak of the pandemic, we suspect the bar is high for a rate cut in 2021.

Norges Bank

2021 has the potential to be a pretty unexciting year for Norwegian monetary policy. That’s not because the economy doesn’t face challenges - the country has imposed new restrictions on socialisation that will undoubtedly halt the recovery and risk a further rise in unemployment.

The interesting question, therefore, is whether the Bank will be one of the first to hike interest rates after the pandemic

Instead, a lack of action from the Norges Bank in 2021 reflects an absence of realistic options to add further stimulus. Negative rates are not seen as a viable option, while logistical constraints mean quantitative easing is unlikely.

The more interesting question, therefore, is whether the Bank will be one of the first to hike interest rates after the pandemic. Clearly, this is unlikely next year, but policymakers are officially projecting the first increase could come in the second half of 2022. While that may seem ambitious given the signals being offered by other central banks, it’s worth remembering that Norges Bank was a key hawkish outlier through 2019 where it hiked rates three times against a more dovish global backdrop.

Download

Download article

17 November 2020

Global Macro Outlook 2021: The darkness before the dawn This bundle contains 15 articles

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more