G10 FX Outlook 2022: Mid-cycle dollar strength

Pandemics and financial crises aside, exchange rates typically can be seen as an extension of monetary policy. They reflect whether central bankers want to hit the accelerator or the brakes. In 2022 it seems clear that the Fed will have the strongest cause to apply some monetary restraint and that the dollar should perform well

Output gaps have closed/are closing

If equity markets embody some sense of confidence in the global economy, then this year’s stellar returns suggest policymakers have achieved their goals in preventing the Covid-19 pandemic from turning into a multi-year recession. G10 economies are bouncing back and concerns about the strength of the recovery are shifting towards unease over the path of inflation.

Output gaps – or how economies are growing compared to potential – can provide some sense on whether central bankers can take their time in normalising loose monetary policy or need to act faster in response to the inflation threat. While output gaps are notoriously hard to forecast, the IMF believes 2022 will see positive gaps in the US (+3.3%) and Canada (+0.8%). In theory, the Fed and the Bank of Canada should be at the front of the queue when it comes to tightening.

The Fed and the Bank of Canada should be at the front of the queue when it comes to tightening

Both the Euro area and Japan have seen negative output gaps since 2008 and probably again in 2022 - justifying the more entrenched dovish positions of those central banks.

Though it seems a very much consensus view, we do favour dollar strength during the Fed lift-off – and largely against those currencies which will be more tolerant of higher inflation. This should mean the EUR, JPY and CHF will be the stand-out under-performers in 2022, while the SEK may lag too.

We do not think a stronger dollar against the low-yielders needs to upset the risk environment yet. After all, it is probably best to characterise the global economy as being in mid-cycle right now – growing confidence in the recovery, inflation picking up and central banks starting up tightening cycles. That should mean most commodity currencies can continue to perform well as their economies realise, through stronger business investment, the benefits of recent terms of trade gains.

GBP probably falls between the three stools of the: i) stronger dollar, ii) weaker low yielders and iii) steady commodity currencies. We think GBP can hold onto its 2021 gains unlike a market generally more pessimistic on the pound.

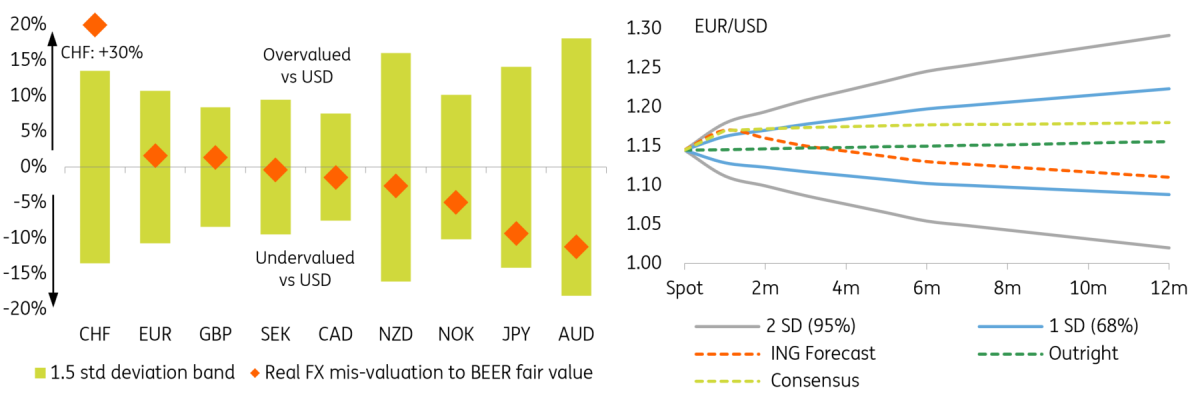

One final point. We do like to drop anchor on some kind of medium-term fair value for currencies against the dollar, using our Behavioural Equilibrium Exchange Rate (BEER) model. Recent terms of trade changes have depressed EUR/USD fair value to around 1.10. That is our year-end 2022 forecast which is well below the consensus of 1.18. Of the under-valued currencies in our BEER model, we would favour NOK and NZD playing catch-up. We are bearish on the JPY in 2022 and whilst the AUD may benefit from being undervalued and over-sold, positioning for recovery here remains a high-risk proposition.

Please see all our regular currency sections below.

EUR/USD - Most roads lead to a stronger dollar

| Spot | Year ahead bias | 4Q21 | 1Q22 | 2Q22 | 3Q22 | 4Q22 | |

|---|---|---|---|---|---|---|---|

| EUR/USD | 1.13 | Bearish | 1.16 | 1.15 | 1.13 | 1.11 | 1.10 |

- Fed cycle under-priced: What turned the dollar around this year was the Fed. Instead of unchanged policy and deeply negative real US rates into 2024, it now looks as though it may hike rates next summer. The Dot Plots have been a big driver here and, even now, money market curves are still some 40-50bp below Fed projections for the policy rate. Good growth momentum going into 2022 (we forecast GDP at 5%) backed by strong corporate and consumer balance sheets should mean that pricing power holds and inflation stays above 3% all year. A stronger dollar can play a role in tightening monetary conditions.

- ECB tightening expectations contained: Pricing of the ECB policy path also fell foul of the energy price shock and at one point nearly 30bp of tightening was priced in for 2022. We view that pricing as extreme and unlikely, although it may take eurozone inflation dipping into next spring (the German VAT hike rolling out of calculations helps) before the market backs away from that kind of pricing. The eurozone is still expected to run a 0.5% of GDP negative output gap in 2022 and the ECB has made it pretty clear it does not want to repeat the mistakes that Trichet made by tightening policy in July 2008.

- Stagflation? The main risk to the above scenario is probably stagflation, where early hikes to address a transitory price shock trigger a recession. The current Fed seems light years away from the Volcker Fed of the early 80s, thus we would see this scenario as unlikely. Even if it were to materialise, stagflation would be negative for risk assets and probably provide support for the anti-cyclical dollar. Perhaps the only scenario for a much stronger EUR/USD in 2022 would be a strong global recovery, a eurozone renaissance (as in 2017) and a Fed turning dovish. With supply chain disruptions expected to weigh on growth in manufacturing-heavy Europe next year, such a scenario seems unlikely.

USD/JPY: Mind the output gap

| Spot | Year ahead bias | 4Q21 | 1Q22 | 2Q22 | 3Q22 | 4Q22 | |

|---|---|---|---|---|---|---|---|

| USD/JPY | 114.50 | Bullish | 113.00 | 114.00 | 115.00 | 118.00 | 120.00 |

- Perfect storm for JPY: The JPY has been the worst-performing G10 currency this year. Driving the JPY weaker has been a reasonably benign environment for risk assets, higher US rates and more recently the energy shock. While our team does see energy correcting lower into next year (Brent to $75/bl), US rates look firmly set to go higher and equities may well stay supported, if not repeating the strong gains of this year. This should keep USD/JPY supported near 115.00, with scope for a break towards 120 as the Fed embarks on its tightening cycle – potentially next summer.

- BoJ happily behind the curve: USD/JPY is certainly a tale of two output gaps. The US economy is expected to run a 2% of GDP positive output gap next year. That means that the Fed may push to the front of the queue when it comes to tightening in the major economies. Despite recent growth, Japan’s economy is still expected to run a 1% negative output gap in 2022 – in other words pricing power is weak. Targeted Japanese CPI is not expected to rise up to 1% until FY23, keeping the BoJ tightly holding its convoluted policy setting of QQE with yield curve control.

- Weak not strong JPY a problem? In early October, the Japanese Finance Ministry seemed to express some concern with the weak JPY. At the time USD/JPY was trading under 112. Concern was, no doubt, related to some sharp moves in FX, but also in an environment of higher energy prices. We suspect Japanese officials will not want to see USD/JPY trading sharply through 115 for the time being, but the combination of a turn in energy lower next spring and the Fed preparing for lift-off suggests 2Q22 could be the topside break-out period for USD/JPY.

GBP/USD: Reports of sterling’s demise look exaggerated

| Spot | Year ahead bias | 4Q21 | 1Q22 | 2Q22 | 3Q22 | 4Q22 | |

|---|---|---|---|---|---|---|---|

| GBP/USD | 1.34 | Neutral | 1.36 | 1.37 | 1.36 | 1.34 | 1.34 |

- BoE policy error? On a trade-weighted basis, GBP is up by more than 3% this year. Yet a common refrain now from GBP bears is that the Bank of England is about to make a policy error. The argument goes that the BoE is set to tighten policy at exactly the wrong moment – akin to President Trichet’s ECB rate hike in July 2008 on the eve of the financial crisis. The difference is that there are no clear signals of a UK recession in 2022. Our economist sees a reasonably healthy UK growth profile next year, initially running at 1% QoQ. That should allow the BoE to hike 15bp this December and a further 50bp in 2022.

- Brexit baggage: GBP bears also point to London’s thorny relationship with Brussels and the risk that the EU-UK Trade and Cooperation Agreement falls apart. Our team’s take on this is a reminder that this agreement is barely better than a No Deal Brexit, such that its failure would not trigger the kind of GBP volatility witnessed in 2019. Additionally, as negotiations have shown, there is plenty of scope for last-minute position adjustment from both sides and we doubt 2022 becomes characterised as a year of looming Brexit deadlines.

- Withstanding the dollar onslaught: It is not a popular view, but we think GBP can withstand the strong dollar onslaught better than some. We doubt Cable has to trade substantially under 1.30 and expect the early BoE tightening to provide GBP with a cushion. In a year when the external environment could become tougher (higher US rates, later in the economic cycle), the UK does not look as vulnerable as some might think. The UK current account deficit has narrowed to a manageable 2% of GDP and the budget deficit is forecast to shrink to just 0.6% of GDP in FY22-23. The UK’s 5-year CDS now trades inside of the US too.

EUR/JPY: Mid cycle support

| Spot | Year ahead bias | 4Q21 | 1Q22 | 2Q22 | 3Q22 | 4Q22 | |

|---|---|---|---|---|---|---|---|

| EUR/JPY | 130.00 | Neutral | 131.00 | 131.00 | 130.00 | 131.00 | 132.00 |

- What of the risk environment? Equity markets (ex-China) have had an excellent 2021. The asset class is seen as an inflation hedge and in theory, should continue to perform well - albeit less spectacularly – in 2022. Typically, equity markets are the last asset class to turn in a business cycle and it seems fair to describe the global economy as shifting to a mid-cycle phase as policymakers remove the punchbowl having grown confident in the recovery. This should be a gently positive environment for EUR/JPY and keep it supported within a 130-134 range.

- Abundant EUR liquidity: Eurozone money market rates should remain depressed near the -0.50% ECB deposit rate through certainly 1H22, although may tick up a little in 2H22 after the ECB’s TLTRO special interest period ends in June. Excess EUR reserves held at the ECB are currently EUR3.6trn and growing. While the ECB will have a challenging meeting on December 16th with regard to how to end the Pandemic Emergency Purchase Programme, we expect a new hybrid scheme to be introduced to smooth the PEPP exit. Like the JPY, we expect the EUR to remain a popular funding currency through 2022.

- Top risks in 2022: Potential risks next year come in the form of geo-political (China-Taiwan/US), (Russia-Europe), financial market (China property crash, Fed over-tightens, EM debt crisis) and social and environmental (New Covid variants, inequality triggers unrest, e.g. Latam, climate events). Invariably at some point, there will be risk-off events that trigger sharp rallies in funding currencies such as JPY and EUR. History would probably suggest that the JPY still outperforms when these risks hit.

EUR/GBP: Unfashionably weak

| Spot | Year ahead bias | 4Q21 | 1Q22 | 2Q22 | 3Q22 | 4Q22 | |

|---|---|---|---|---|---|---|---|

| EUR/GBP | 0.845 | Mildly Bearish | 0.85 | 0.84 | 0.83 | 0.83 | 0.82 |

- Brexit risk premium smaller: As above, we doubt the noise regarding the unravelling of EU-UK trade negotiations has to hit GBP as hard as it did in 2019. Back then, GBP traded with a 5-6% risk premium to the EUR. In other words, we doubt EUR/GBP has to spike 5-7 big figures on any substantial deterioration in cross-channel relations. Based on how GBP has traded so far this year, we believe Brexit fatigue can keep the risk premium more to the 1-2% region. 0.8650/8700 could then remain at the top of the EUR/GBP trading range.

- ECB-BoE divergence: Inflation looks set to rise in both the UK and the eurozone over the coming months. Eurozone CPI should peak this December at around 4.3%, but the UK highs shouldn't come until April and higher at 5%. Despite market pricing to the contrary, an ECB hike looks highly unlikely next year and abundant liquidity (pressing market rates to the deposit rate floor) looks set to remain well into 2023. In the UK, we are faced with the intriguing prospect of the BoE allowing its Gilt holdings to roll off once the policy rate hits 0.50%. The improvement in relative government bond yields should favour GBP.

- Politics: The FX options market attaches a sizeable risk premium to the French elections next April, particularly the run-off on April 24th. President Macron looks comfortably ahead in the polls at present with around 25% of the vote, though plenty can change over the next six months. French elections certainly weighed on the euro in early 2017. In the UK, the Johnson government seems to survive most missteps and the opposition Labour party are yet to mount a serious challenge. And we suspect Chancellor Rishi Sunak is keeping his powder dry for a pre-election tax give-away potentially in early 2023. Arguably, therefore, political risks are greater for the eurozone in 2022.

EUR/CHF: Testing the SNB’s tolerance

| Spot | Year ahead bias | 4Q21 | 1Q22 | 2Q22 | 3Q22 | 4Q22 | |

|---|---|---|---|---|---|---|---|

| EUR/CHF | 1.05 | Bullish | 1.05 | 1.07 | 1.08 | 1.10 | 1.12 |

- Hedging inflation with the Swiss Franc?: The CHF has surprisingly been one of the biggest beneficiaries of the autumn energy price spike. The argument goes that with very low inflation in Switzerland, everyone else’s real interest rates (nominal less inflation) have come lower – thus making the CHF more attractive. We think there are probably other factors at work here too. Switzerland’s trade balance remains strong (surpluses in excess of CHF4bn per month since May) and continued ECB money printing is keeping EUR/CHF subdued. EUR excess reserves parked at the ECB are now EUR3.6trn!

- Looking for SNB’s line in the sand: The SNB retains a policy stance of rates at -0.75% and continued FX intervention to fight the ‘highly valued’ CHF. The SNB will be reluctant to draw a line in the sand, e.g. 1.0500, to try and defend. We note that the real trade-weighted CHF remains 5-6% off its 2015 highs, suggesting that if the SNB is to throw the kitchen sink at EUR/CHF, it may not be until it gets closer to 1.00. The reason for continued intervention is that the SNB still sees Swiss CPI less than 1% in 2024 and has more reason than many to hold into its dovish stance.

- Testing the SNB’s resolve: Like the Bank of Israel, the SNB’s commitment to fighting currency strength is being tested. Even though the SNB’s balance sheet is now greater than CHF1trn, there seems no domestic pressure to stop growing FX reserves. Instead, the pressure comes from investors wondering whether: a) the SNB will become less concerned about deflation and more tolerant of CHF strength and b) the US Treasury has effectively warned the SNB off intervention. As above, we very much doubt the SNB does a U-turn in policy in 2022 and would expect a slowing in ECB balance sheet expansion to start providing EUR/CHF with support as 2022 progresses.

EUR/NOK: Still a bright outlook for the krone

| Spot | Year ahead bias | 4Q21 | 1Q22 | 2Q22 | 3Q22 | 4Q22 | |

|---|---|---|---|---|---|---|---|

| EUR/NOK | 9.89 | Bearish | 9.85 | 9.75 | 9.70 | 9.60 | 9.50 |

- Energy story: NOK has already benefitted in the past few months from being a large energy exporter, but the positive implications for the Norwegian economy are likely there to stay, as rising investments in the energy industry are set to further underpin the recovery. We expect only a gradual decrease in oil prices in 2022 (Brent to average: 76$/bl), which should partly offset the sharper contraction we expect in natural gas (TTF to average 39 €/Mwh in 2022). We must remember that, unlike other exporters, Norway’s low hydro reserves makes it prone to a sharp rise in domestic energy costs. There is a non-negligible risk that the country may face a situation where higher costs of living may coincide with wider room for wage increases as investments rise and the job market tightens; the result could be a considerable heat-up of the economy and inflation.

- Norges Bank to stay hawkish: We think the growth and inflation outlooks will continue to support the Norges Bank’s tightening plans, which currently imply three hikes in 2022 after the already announced hike in December. The market pricing is broadly replicating the NB's latest projections. We think the risks are skewed towards the central bank overdelivering (four hikes in 2022); as highlighted in the point above, we see some risk that the economy may heat up excessively in early 2022, which could lead the NB to accelerate its tightening plans. Still, even with three hikes next year, a policy rate at 1.0% means that NOK will be at the forefront of benefitting from any revamp of carry trade interest in G10.

- Risk environment and valuation: NOK is the least liquid G10 currency and has the highest sensitivity to swings in global equities, so our bullish views on NOK rely on the assumption that global tightening cycles will not generate a persistently risk-averse environment in markets next year. Despite this year’s extended downtrend, EUR/NOK is still around 7% overvalued according to our medium-term BEER model, and we see room for a move to 9.50 by 4Q22.

EUR/SEK: Waiting for the Riksbank’s delayed hawkish turn

| Spot | Year ahead bias | 4Q21 | 1Q22 | 2Q22 | 3Q22 | 4Q22 | |

|---|---|---|---|---|---|---|---|

| EUR/SEK | 10.04 | Mildly Bearish | 10.00 | 9.90 | 9.85 | 9.75 | 9.65 |

- Riksbank playing it cool: The market is currently pricing in around 50bp of monetary tightening by the Riksbank in 2022. We think such hawkish expectations are unwarranted given a relatively subdued medium-term inflation outlook in Sweden. We expect no hikes before 2023, and we think the RB will push back against the market’s hawkish bets in November and possibly until early-2022. Still, tightening plans elsewhere and a robust domestic story should force a hawkish shift in communication by 2H22, which should take the form of signals about balance sheet reduction and/or some 2023/24 hikes being added in the rate projections. Still, lower rate attractiveness suggests SEK will struggle to outperform higher-yielding currencies like NOK in periods of supported risk sentiment.

- Global trade recovery: Sweden is a very open economy (total trade-to-GDP ratio was around 60% before the pandemic) and its economic fate is heavily tied to the recovery in global trade. Our trade team expects global demand to stay strong, while supply strains may keep hindering the trade rebound in 1H22 before easing in 2H22. We expect a YoY increase in global trade by 2.9% in 2022. More than half of Swedish exports are intra-EU and while we don’t see eurozone growth exceeding expectations, we still forecast a decent 3.9% YoY for 2022, which should keep supporting the Swedish export industry.

- Valuation and historical considerations: From a valuation point of view, EUR/SEK is fairly valued in the medium-term according to our BEER model. We see room for some overshoot on the undervaluation side in the next couple of years, which incidentally was the case in the post-GFC recovery when EUR/SEK dropped below 9.00 and was moderately undervalued until 2013. Back then, an aggressive Riksbank tightening cycle gave an extra boost to SEK. As this is unlikely to happen this time around, we expect SEK gains to prove more moderate. We target 9.65 in EUR/SEK for the end of 2022.

EUR/DKK: More FX interventions, but another cut not very likely

| Spot | Year ahead bias | 4Q21 | 1Q22 | 2Q22 | 3Q22 | 4Q22 | |

|---|---|---|---|---|---|---|---|

| EUR/DKK | 7.437 | Neutral | 7.44 | 7.44 | 7.44 | 7.45 | 7.45 |

- Monetary/FX policy: The Danmarks Nationalbank intervened for DKK 74.5bn in the FX market to defend the EUR/DKK peg before deciding to cut the deposit rate from -0.50% to -0.60% on 30 September. The positive impact on EUR/DKK has faded since then, and after peaking at 7.4410, the pair has now moved back to the middle of the 7.4350/7.4400 area. This may signal how the wider EUR/DKK rate differential may be a necessary but not sufficient driver for consistent re-appreciation in the pair, given current market conditions. At the same time, the differential should be able to provide a floor that is solid enough to let the DN manage the peg only with FX interventions and not with another rate cut in 2022. A potential shift to a more hawkish tone by the ECB in the second half of 2022 may also provide some support to the pair, but we may have to wait until late 2022 or even 2023 to see the pair stabilise in the 7.4500/7.4600 region.

USD/CAD: Loonie is the safest commodity currency

| Spot | Year ahead bias | 4Q21 | 1Q22 | 2Q22 | 3Q22 | 4Q22 | |

|---|---|---|---|---|---|---|---|

| USD/CAD | 1.255 | Bearish | 1.24 | 1.23 | 1.22 | 1.21 | 1.22 |

- Commodities and external factors: We expect oil to average 76$/bll (Brent) in 2022, with a gradual return to surplus driving prices moderately lower. Such a gradual downtrend should not be enough to undermine the recovery in the Canadian oil and gas industry, currently a major driver of economic strength. Being a very open economy, Canada is also set to benefit from the further recovery in global trade, which could accelerate in 2H22 as supply strains ease. As 70% of Canada’s exports head to the US, long-CAD should continue to be a proxy trade for the strong US growth story.

- Strong domestic economy: In Canada, the jobs market is at pre-pandemic levels, record-level investments keep supporting the growth outlook and a very successful vaccination campaign is allowing a loosening of the so-far very strict border policy. When adding that demand from the neighbouring US for Canadian exports is likely to keep rising, and Trudeau’s government pledged to keep fiscal policy loose for longer, the domestic economic story is set to remain a positive for CAD, and partly shield it from any risk-off waves or USD appreciation.

- BoC to act fast: The Bank of Canada shifted to a more hawkish stance in October by ending QE and signalling a first hike should come in 2Q22 or 3Q22. Markets are currently pricing in the first hike at the March meeting and see a total of 125bp of tightening in 2022. We currently forecast four 25-bp rate hikes in 2022, so expect only limited scope for a re-pricing of tightening expectations. Having the lowest volatility among G10 commodity currencies, CAD may emerge as a popular carry bet against low-yielders next year. We think CAD has the lowest downside risk in the commodity FX space and expect USD/CAD to stay closer to 1.20 rather than to 1.25 in 2022.

AUD/USD: Room to rise, but big downside risk

| Spot | Year ahead bias | 4Q21 | 1Q22 | 2Q22 | 3Q22 | 4Q22 | |

|---|---|---|---|---|---|---|---|

| AUD/USD | 0.73 | Mildly Bullish | 0.73 | 0.73 | 0.74 | 0.74 | 0.75 |

- Monetary policy outlook: The RBA dropped its yield-curve-control policy in November but has retained dovish forward guidance to 2024. The lockdown-induced period of soft data should not last much longer and a 70% vaccination rate reduces the risk of new restrictions. We expect a solid rebound in unemployment and while a sharp rise in wage growth is not guaranteed, inflation should remain within the 2-3% RBA target in 2022. The growth outlook is blurrier as many headwinds may come from China. We think the RBA will taper asset purchases and end QE before the end of 2022. The first hike may only come in early 2023, although risks are skewed towards an earlier move. Still, the market pricing (75bp of tightening in the next 12 months) is too hawkish in our view.

- Commodities: AUD has benefitted from Australia’s energy-exporting industry (around 20% of all exports), but our commodities team expects natural gas and coal (Australia’s second and third biggest exports) to be among the main victims of the energy price decline in 2022 – especially in the first half - and average 39 €/Mwh (TTF) and 110 $/t (Newcastle coal) in 2022. Iron ore (Australia’s primary export), whose prices have approximately halved since mid-2021, should be able to hold around the current $100 levels on average next year, although a return to the 1H21 levels appears off the cards given China’s new restrictions on steel production. All in all, we expect a moderate net-negative impact of commodities on AUD in 2022.

- Valuation and positioning are supportive: The market is pricing in too much RBA tightening in our view, but AUD still has to catch up with the recent hawkish re-pricing. Incidentally, AUD is the most undervalued (-11%) G10 currency against the USD, according to our medium-term BEER model. AUD is also the most oversold currency in G10 and has the widest room to benefit from short squeezes in risk-on periods. Still, AUD is arguably facing the biggest deal of downside risks among G10 commodity currencies given its huge exposure to China-related sentiment and a potential commodities downturn. Even assuming only very few of those risks materialise, a return to the 2021 0.80 highs in AUD/USD seems quite unlikely in the next year.

NZD/USD: Counting on a strong domestic story

| Spot | Year ahead bias | 4Q21 | 1Q22 | 2Q22 | 3Q22 | 4Q22 | |

|---|---|---|---|---|---|---|---|

| NZD/USD | 0.70 | Bullish | 0.70 | 0.71 | 0.72 | 0.73 | 0.74 |

- An aggressive RBNZ: The RBNZ is one of the most hawkish central banks in G10, and markets are pricing in around 175bp of tightening between now and the end of 2022. We think hawkish expectations are overdone, as we expect 125bp of tightening (100bp are already embedded in the RBNZ’s latest rate projections). We think markets will have to scale down tightening expectations for 2022, but signs of persistent inflation throughout the year should fuel speculation that the tightening cycle will have to continue in 2023-24, and put a floor below NZD. The currency should have the most attractive carry in G10 in the year ahead and should therefore benefit more than others from periods of low volatility a supported risk sentiment.

- Strong domestic economy: The RBNZ tightening should be supported by the strong domestic economy story. After likely facing some drag from the recent lockdown in Auckland, the vaccination programme should allow some gradual re-opening of borders. A rebound in tourism and education – two key sectors for the NZ economy - are set to give an extra boost to the economy. Given the exceptionally tight jobs market, inflationary pressure appears to have a less transitory nature than elsewhere in the developed world, even though easing housing and energy prices in 2022 should allow some normalisation.

- Mixed external environment: New Zealand commodity exports are almost solely in dairy and agriculture products. While not experiencing the same kind of rally seen in energy commodities, milk and forestry prices (the two main exports) are still considerably higher than in the last five years, and even in case of a correction in 2022, the exporting industry should continue to underpin the recovery. A big downside risk for NZD in 2022 is, however, China-related sentiment, which remains quite uncertain amid government crackdowns on some sectors and a potential economic slowdown. While being modestly undervalued vs USD in the medium term (3% according to our BEER model), NZD is the most overbought currency in G10 and is facing some position-squaring-related downside risk in the near term. We expect NZD/USD to rise gradually to 0.74 in 2022.

Download

Download article

17 November 2021

2022 FX Outlook: Liquid Allsorts This bundle contains 7 articlesThis publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more