Czech headline inflation remains unchanged

Headline inflation remained elevated in November, but core inflation softened marginally. Worries about above-target inflation next year or the lukewarm economic recovery will drive the upcoming decision about a pause or another cut. Still, real interest rates are drifting lower while wage growth and spending remain robust

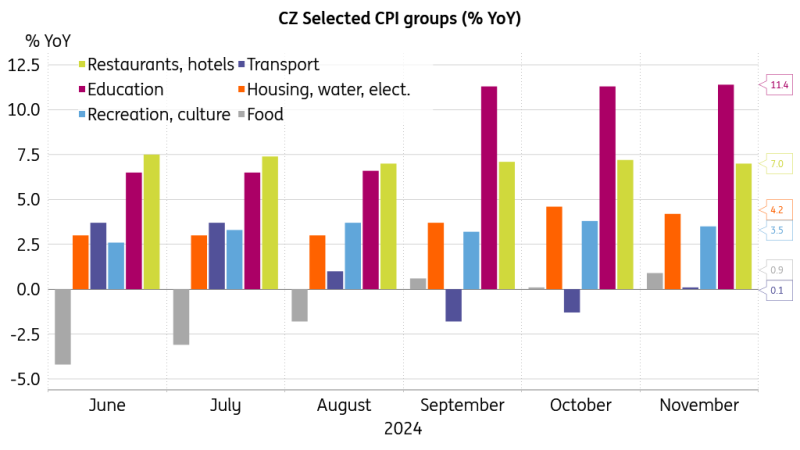

Food prices drive inflation, while alcohol and tobacco are a drag

Czech annual inflation remained stable at 2.8% in November. Prices in the food section had the most potent positive effect on overall price dynamics, with prices in the milk and eggs group flipping to 4.3% annual growth in November from a decline previously. In contrast, a slowdown in annual price gains was noticeable for alcoholic beverages and tobacco, and clothing and footwear prices dropped more when compared to the preceding November. Annual price dynamics also softened in the housing section, with the electricity price increase easing to 9.2% year-on-year in November (10.5% previously) and gas prices falling 2.9% YoY in the same month (down 2.3% previously).

Imputed rents rose by 1.5% YoY in November (1.7% previously), mainly due to the rise in new house prices. In aggregate, prices of goods added 1.4% from the previous year, while services prices increased by 5.2%. Core inflation has softened to 2.3% in November, coming in slightly below the Czech National Bank's forecast. Indeed, annual growth of more volatile items of the consumer basket, such as food and transport, turned positive in November, while price dynamics of less fluctuating items, such as restaurants and recreation services, moderated.

Price growth softened for core inflation items

In monthly terms, consumer prices picked up by 0.1%, with higher prices in the food section being the main driver of the monthly gain. The 23.3% increase in egg prices from the previous month was the most pronounced growth factor; prices of fuel and oil added 0.8% month-on-month. In contrast, the alcoholic beverages and tobacco section was the main negative contributor to overall monthly price dynamics, with spirits prices shedding 2.1% MoM.

Pause or another cut – which side to choose?

The latest inflation print is below the CNB Autumn Forecast and market expectations, providing policymakers with some relief for their upcoming meeting. The decision will be made between a pause in the current cutting cycle and a further 25bp rate cut. The outlook for above-target inflation next year calls for a pause, while more support for the lukewarm economic rebound amid weak investment calls for further easing in the monetary policy stance. The next moves and the views of the European Central Bank and Federal Reserve will also enter the CNB's decision function and shape the outcome of the approaching vote. It will be a close call, yet we see a pause in December as the more likely option, with easing likely to resume in March after January’s inflation data is out.

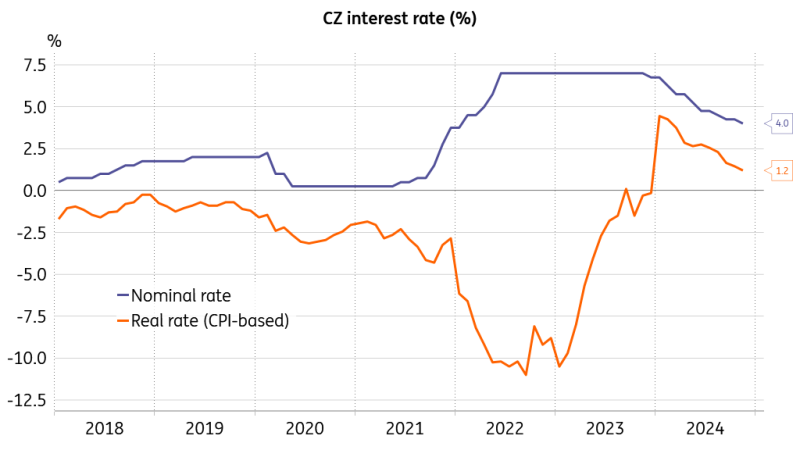

Both nominal and real interest rates drift lower

The real interest rate has declined since the beginning of the year, currently approaching 1.2%. Should the consumer price dynamics rise above 3% in December and remain elevated over the next year, real interest rates could easily slide below 1% and stay there for longer. In conditions of lofty nominal and real wage growth, combined with continued household spending, it does not seem clear-cut that the disinflation in the service sector can carry on. On the other hand, should the economic prospects for Europe deteriorate further and German industry fail to hit bottom, the Czech economic rebound would come under more pressure. Whether the economic malaise in Europe is driven by high borrowing costs or deeply-rooted structural issues might be difficult to disentangle. Still, we lean more towards the second option as low real interest rates can only do so much.

Download

Download articleThis publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more