Credit Supply Outlook: The Collection

Credit supply forecasts are mixed for 2024. We expect higher supply in EUR corporates and financials, ESG supply, high yield and Real estate supply. However, we forecast lower Reverse Yankee supply, corporate hybrid supply and covered bond supply. Meanwhile, USD corporate supply should remain stable

We forecast €310bn in EUR corporate supply in 2024

We are forecasting a minor increase in corporate supply in 2024, but overall low supply. The main driver of this increase is the rise in redemptions from €246bn up to €260bn. Thus, net supply remains low at just €50bn. The technical picture, therefore, remains strong.

Net supply remains low in 2024

Why we expect a small increase in supply but overall low supply:

Higher for longer rates

Rates are likely to stay at these elevated levels for some time and come down slowly. Our rates strategists expect EUR rates to move mostly sideways in the coming year, with EUR 10-year swap rates only dipping towards 3% by the middle of next year from around 3.25% currently. As such, funding costs remain very high. However, in saying that there has been a strong preference for issuers to hold off new issuance until next year in an attempt to get cheaper funding with the expectation of rates falling.

Less availability of credit and equity

With tighter lending standards, less available bank liquidity and banks looking to reduce exposure to risk, many corporates will be pushed towards the bond market. This adds some additional supply pressure, particularly in certain segments of the market. Additionally, there is now a lack of access to IPOs, LBOs and private equity, further putting pressure on corporates' ability to refinance.

Expect disintermediation trend to remain

We expect a small increase in supply due to the continuing disintermediation trend. As shown in the chart below, there has been a trend of more disintermediation over the past ten years. 2023 is likely to function like 2012 and 2016 when supply increased following a year of low bond supply relative to loan supply (ratio of loans-to-bonds in 2012, 2016 and 2022 all increased, breaking the disintermediation trend due to market volatility but rebounded the subsequent year).

Disintermediation trend to remain

Decreased cash buffer

The significant cash levels on the books of many corporates (due to large funding done in 2019-2021) have been depleted, and thus the buffer is lower. This means refinancing costs could increasingly become a problem in 2024, particularly for high-yield issuers and real estate issuers. This also creates an element of urgency to get funding done.

Low Reverse Yankee supply expected

Much like this year, we don’t expect Reverse Yankee supply to play a dominant role. Thus, we are not likely to see additional supply pressure coming from US issuers. As elaborated on below, we forecast just €40bn in 2024.

Low Corporate hybrids supply expected

Similarly, looking at Corporate hybrids, we also don’t expect a large level of supply. On the back of still very high refinancing costs, we are forecasting only €15bn in 2024, as detailed below.

Insignificant volume of assets and liabilities management exercises expected

An insignificant volume of assets and liabilities management exercises are expected in 2024, as the current high-yielding environment and wide spread levels leave very little attraction.

Low M&A activity expected

We expect M&A activity will remain at low levels in the first half of the year, and perhaps pick up in the second half of the year.

Small rise in CAPEX is forecasted

CAPEX levels are expected to rise in both EUR and USD IG, as shown below. The rise is indeed marginal but does play a role in the expectation of a small increase in supply. The growth in CAPEX is very much driven by Financials, Energy, Industrials, Utilities and Consumers.

Small rise in CAPEX in coming years

Sector breakdown of corporate supply

We forecast €483bn in EUR financial supply in 2024

We forecast €180bn in EUR covered bond supply in 2024

We forecast €125bn in EUR preferred senior supply in 2024

We forecast €110bn in EUR bail-in senior supply in 2024

We forecast €28bn in EUR T2 supply in 2024

We forecast €12bn in EUR AT1 supply in 2024

Five factors driving bank bond supply next year:

1. At best sluggish lending volumes

The banking sector has felt the impact of a slowing economy and higher rates in 2023. Private sector lending has been sluggish, and lending books have declined to slightly below the levels seen at the end of the year, both for households and corporates. Consumer credit has held up better, offsetting part of the decline in loans for house purchases.

With the (very) limited economic growth pencilled in for 2024, we expect lending to remain subdued in 2024. This will set a cap on balance sheet growth and limit additional bank funding needs.

2. Less reliable deposit developments

Deposit balances have been more harshly hit than lending balances in 2023 in the eurozone, particularly in Italy, Spain and France. In 2024, alongside less impressive lending, we also expect deposits to remain under pressure.

Furthermore, higher interest rates continue to drive depositors into better-yielding alternatives, reflected as an ongoing shift from current accounts into term deposits. More active depositors and more competition for deposits mean it is less straightforward for banks to rely increasingly on deposits for funding.

Eurozone banks have increased their share of deposit funding in the past couple of years, supported by the generally stable nature of deposits and their beneficial regulatory treatment. We would not take it for granted that this trend will continue as it has in the current environment.

3. End of the ECB funding support for banks

Bank funding needs are likely to remain substantially impacted by the runoff of European Central Bank funding. Another €450bn in Targeted Longer-Term Refinancing Operations mature in 2024.

A substantial share of the excess Liquidity Coverage Ratio liquidity buffers have already been exhausted. While there is still further headroom to absorb the additional impact, we see a higher risk for refinancing maturing LTROs, in particular for banks in Italy and Germany. Part of the refinancing is likely to continue to head to bond markets, subject to market circumstances remaining accommodative. We wrote about the LCR impact of the LTRO runoff here.

As the ECB is seeking to bring down the excess liquidity in the system, it would be highly controversial for it to offer banks the option to lengthen these drawings into a new longer-term refinancing operation, in our view. We do, however, expect part of these funds to end up being rolled over in the shorter operations, including the three-month Longer-Term Refinancing Operations and Main Refinancing Operations. However, we think some stigma may be attached to this and as such, the bulk of banks would likely seek to find other sources of funding to replace their central bank drawings.

4. Bond redemptions remain broadly stable

Bank bond redemptions are set to remain broadly stable year-on-year in 2024, reaching just above €290bn. Of these, €121bn are in covered bonds, €145bn in senior debt and €27bn in bank subordinated paper.

The largest changes in redemptions are seen in bail-in senior debt, where redemptions could increase by €15bn YoY. Preferred senior debt maturities are seen c.€15bn lower YoY, and covered bonds could see lower redemptions of €5bn YoY. Subordinated debt redemptions could increase slightly YoY, driven by higher Tier 2 redemptions and calls and a stable amount of AT1 debt with first call dates in 2024.

5. Bail-in senior markets reach a more mature stage

Bail-in senior issuance in 2024 will be driven by a combination of potential risk-weighted asset changes that may impact the total MREL (minimum requirement for own funds and eligible liabilities) eligible debt needs and redemptions.

We see that the bail-in senior market is reaching a more mature stage. Larger banks are already meeting their loss absorption requirements.

While lending is likely to remain pressured, we expect that regulatory changes will continue to impact risk density and may push RWA higher.

On top of this, there are limited MREL shortfalls in smaller institutions. Banks in jurisdictions with a longer MREL transitioning time have some further work to do to meet their MREL requirements. Greek banks are among those that have some further work to do with another c.€8bn to meet their MREL requirements.

Balance sheet changes and MREL shortfalls as supply drivers

What to expect in terms of bank bond supply in 2024

We expect bank bond supply to remain high in 2024, reaching €455bn. And bank net supply remains elevated.

While the increase in the overall funding needs is perhaps limited by sluggish lending volumes, we don’t expect the share of deposits to continue to head higher, and banks will continue to refinance part of their maturing LTROs via the bond markets.

We expect the LTRO refinancing wave to result in heavier supply landing in the first quarter of 2024.

We expect unsecured bank bond supply to remain elevated in 2024, offsetting the impact from lower covered bond supply

Senior unsecured supply to offset the slump in covered bonds in 2024

We forecast higher senior unsecured issuance to offset the slightly lower covered bond reading that we pencil in for 2024. Preferred senior debt issuance will likely remain solid at €125bn, while covered bond issuance will edge lower to €180bn. We think preferred senior debt and covered bonds will be the most fitting longer-maturity funding alternatives for banks seeking to refinance their LTROs.

The share of bail-in senior to total senior issuance has declined year-to-date to 49% from 57% in 2022. The change has been driven by the substantial increase in preferred senior debt issuance. We expect the share of bail-in senior debt to total senior debt to slightly decrease further next year. We forecast bail-in senior supply to reach €110bn in 2024.

In 2023, banks have issued €194bn in senior debt, of which €99bn was in preferred/OpCo debt and €95bn was in bail-in senior debt (NPS/HoldCo) on a year-to-date basis. The supply is running substantially ahead of last year at this time when senior issuance reached €157bn, split between €69bn in preferred and €88bn in bail-in senior debt.

We expect covered and senior issuance to remain ahead of redemptions again in 2024

In bank capital, banks start to gear up for higher redemptions to come

We forecast that 2024 should see solid bank capital supply. We forecast that bank capital issuance will reach €40bn in 2024, split between €12bn in AT1 and €28bn in T2. This is a step higher from 2023, for which we forecast €33bn total, with the YTD levels running currently at €29bn.

Redemptions will drive capital supply higher in 2024, in our view. Alongside the 2024 redemptions, we think issuers will be getting ready for the higher redemption burden approaching in 2025. Euro-denominated bank capital redemptions will increase by €3bn YoY to €27bn in 2024 and further to €43bn in 2025.

We believe that the timing of capital issuance is largely impacted by market conditions. If market conditions were to remain volatile, banks would be more likely to jump on any issuance window on a more proactive basis. If, instead, the market views of 2025 turn out to be more upbeat, banks may feel more comfortable waiting to refinance their early 2025 redemptions closer to the actual call dates. We think banks will generally seek to call their capital at the first call date instead of extending the notes.

Bank capital issuance to remain ahead of redemptions in 2024

In euro-denominated AT1, €5bn in (originally) benchmark size AT1 debt outstanding has the first call date in 2024. This includes c.€400m for the two deals that have been tendered in 2023 ahead of the 2024 calls. On top of this, €1.8bn in sub-benchmark debt is callable in 2024.

AT1 redemptions will substantially increase in 2025 to €15bn, of which €12bn is in benchmark size. Part of the 1H25 calls may be refinanced already in 2024.

Redemptions will also increase in Tier 2 debt. A further €18bn is set to reach its first call date in 2024 in callable Tier 2 debt, of which €14bn is in benchmark size, while €1.9bn bullet T2 matures. T2 bullet redemptions increase to €10bn in 2025 and callable T2 repayments remain stable at €18bn in 2025. Due to the limited remaining capital recognition of outstanding bullet T2 debt one year prior to the maturity, these deals may be partly replaced by bail-in senior as here; regulatory capital recognition is likely less of a driver.

Financial bond supply forecats

We forecast US$650bn in USD corporate supply in 2024

We expect USD corporate supply will be more or less in line with this year’s supply, which we expect to approach US$650bn – despite seeing redemptions falling next year from US$526bn down to US$469bn. This will result in an increase in net supply up to US$181bn, still lower than some previous years (2016-2021).

Small increase in net supply in 2024, but still overall low

We believe supply will remain in line with this year due to:

Higher for longer rates

Rates are likely to stay at these elevated levels for some time, and come down slowly. Our rates strategists expect USD 10-year swap rates have more room to rally; they are also likely to dip below 3% next year, but only temporarily. As such, funding costs remains high, but does fall slightly.

Many corporates holding off for the fall in rates

With Fed rate cuts closer in sight, many corporates have purposefully postponed issuance until 2024 in hopes of falling rates and cheaper funding. Our economists expect a Fed rate cut in the first quarter of 2024.

Lower redemptions pencilled in for 2024

A main driver for not seeing a major increase in supply in 2024, as our forecast does still sit below the historical average of US$700-750bn, is the drop in redemptions from US$526bn down to US$469bn, thus less refinancing.

M&A levels will remain low initially

We expect M&A activity will remain at low levels in the first half of the year and perhaps pick up in the second half of the year.

Low Reverse Yankee supply expected

Much like this year, we don’t expect Reverse Yankee supply to play a dominant role. Thus, we will see issuers focussing domestically in the USD bond space. This adds slightly to the equation of supply, countering the drop in redemptions. As elaborated on below, we forecast just €40bn in 2024.

We forecast €15bn in corporate hybrid supply in 2024

Much like in 2022 and 2023, we are expecting relatively low corporate hybrid supply in 2024. We are forecasting €15bn for next year, below the €24bn being called. Normally we would look at half of the coming year’s calls and half the following year’s calls in order to estimate the pure refinancing levels. This would then equate to €25bn for 2024. We think other factors will dominate and keep the supply lower, albeit up on 2023 and 2022, due to the rise in calls in 2024 and the slow fall in rates expected.

- Very high funding costs for hybrids will remain

- Issuers can call or tender and not replace

- Many issuers have already refinanced callable bonds in 2024

- Without losing equity, credit issuers can tender 10% of their outstanding hybrids

- If an issue is NOT called, it will lose equity credit. But the rest of the hybrid curve by the same issuer does not

- If an issuer calls but does not replace, then equity credit is moved to minimal on all hybrid issues

- The lower the coupon (or more exactly said the lower the initial credit spread component of the initial hybrid issue) the less likely the issue will be called in the current high-yield environment

- Issuers have other stakeholders to consider, thus refinancing at any level is not always a realistic option

- On the contrary, we expect a small rise in hybrids as many of the aforementioned alternative options have been somewhat exhausted by some issuers, thus some will have to bite the bullet and refinance.

Hybrid supply to rise, but remain lower than calls in 2024

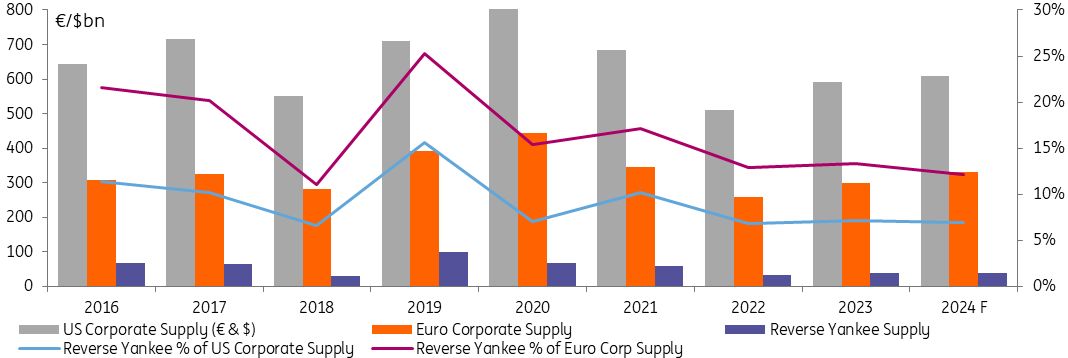

We forecast €40bn in Reverse Yankee supply in 2024

We are not expecting a large influx of Reverse Yankee supply in 2024. We forecast just €40bn in 2024, in line with what we have seen this year. We will see a drop in Reverse Yankee redemptions next year, down to €40bn, thus we expect flat net supply.

Expect a drop in Reverse Yankee supply

The equation for Reverse Yankee supply is not favourable for a cost-savings advantage at this time. While our rates strategists believe the cross-currency basis swap will continue to trade around these levels, we do expect USD spreads will continue to outperform overall against EUR. As shown below, the USD EUR spread differential is at rather tight levels, whereas USD non-financials trade relatively rich. Furthermore, there may be more room for performance in USD due to the higher likelihood of a soft landing.

Cross currency basis swap & USD EUR spread differential - 5yr

Cross currency basis swap & USD EUR spread differential - 10yr

Lastly, Reverse Yankee supply is normally a factor of total supply by US corporates and total Euro corporate supply in a given calendar year.

We forecast US corporate supply (in $ and €) to be up in 2024 compared to 2023. We forecast US corporate supply will also be above the normal 93% of USD corporate supply in 2024, as we expect more issuance will be done domestically. Thus, we forecast US corporate supply (in $ and €) to reach US$610bn. Similarly, we forecast an increase in EUR corporate supply up to €310bn.

Historically, Reverse Yankee supply generally accounts for around 10% of US corporate supply. However, due to market circumstances and expecting lower Reverse Yankee supply, we expect it will account for 7%, in line with what we have seen in 2022 and 2023. Similarly, Reverse Yankee supply would normally account for about 19% of EUR corporate supply, but we expect it will also be more in line with the previous two years and account for just 12%, with our forecast of €40bn for 2023.

Reverse Yankee supply as a % of US corporate supply and EUR corporate supply

We forecast €90bn in EUR corporate ESG supply in 2024

After a disappointing 2023, corporate ESG € supply will grow moderately

Year-to-date, corporates (including real estate) have issued c.€75bn of green, sustainability, social and sustainability-linked bonds (SLB). We initially expected a stronger issuance around €100bn for the full year 2023, but €80-85bn is probably the maximum amount we will see by the end of the year.

Year after year, the green bond framework format reaffirms its leadership on the market. Year-to-date, corporates’ ESG issuance has been dominated at 69% by green bonds. Sustainability-linked bonds (SLB) maintain a 30% share. The remaining 1% is a social bond issued by Motability Operations Group.

| €90bn |

Expected Corporates’ ESG € bond supplyIn 2024 |

With global corporate IG € supply up c.€20-30bn in 2024 vs. 2023, to c.€310bn, we forecast corporates ESG IG € around €90bn for 2024. We believe that green bonds will retain a share of around 70%. The market has not yet seen a corporate sustainability bond issued in 2023 thus far, but the instrument could reappear on the market in 2024, still representing a tiny part of total corporate ESG issuance.

Corporates IG € ESG bonds 2019 – 2024F

The total share of ESG bonds within corporates’ € total supply has increased year after year from 4% in 2018 to 35% in 2022. 2023 marks a retrenchment of the ESG bond share with 27% year-to-date. With an expected corporate € supply of around €310bn in 2024 due to higher redemptions and an ESG supply that we forecast at €90bn, ESG bonds should maintain a 27% share next year.

Corporates ESG IG € bond share in total corporate bond supply 2018 – 2024F

Inflation and projects pipeline can explain the ESG bond supply weakness

Corporates’ ESG issuance was extremely strong in 2021 and 2022, with notably a lower interest rate environment that boosted bond supply. Corporates need the time to allocate the proceeds to new green projects. Therefore, 2023 and 2024’s ESG issuance suffers from the existing projects pipeline.

With higher interest rates and higher costs of materials, most sectors have curbed their capital expenditure ambitions in 2023 (although still growing vs. 2022). This is particularly the case of the real estate sector, which has concentrated its efforts on balance sheet management in an environment where asset valuations were negatively impacted. Globally, for most industries, next year will see another capex growth reduction compared to 2023.

Automotive, Utilities and Real estate seen active on the ESG € market in 2024

Accounting for 58% of total corporate ESG € issuance YTD, industrials have already surpassed their issuance for the full year 2022. The sub-sectors automotive, transport and aviation have used the market intensively thus far in 2023. We see this as a catch-up momentum with transport and aviation activities coming back to speed after the Covid-19 pandemic restrictions. As far as the automotive sector is concerned, we think that ESG issuance level is here to stay, with the industry gearing towards more sustainable car models.

Utilities should continue to be important players for the ESG bond market, with issuance representing about 30%. The sector and its transition towards green energy production and transmission will continue to have a large pipeline of green projects for the coming years.

Real estate’s bond supply has been extremely small this year and ESG issuance has been almost non-existent. In 2022, the sector issued €11bn of ESG bonds. The negative impact of higher interest rates and costs of material has shifted real estate companies’ intention to balance sheet management. Depending on the evolution of inflation and interest rates in 2024, we could see the sector coming back to the bond market and playing a more important role in the ESG markets.

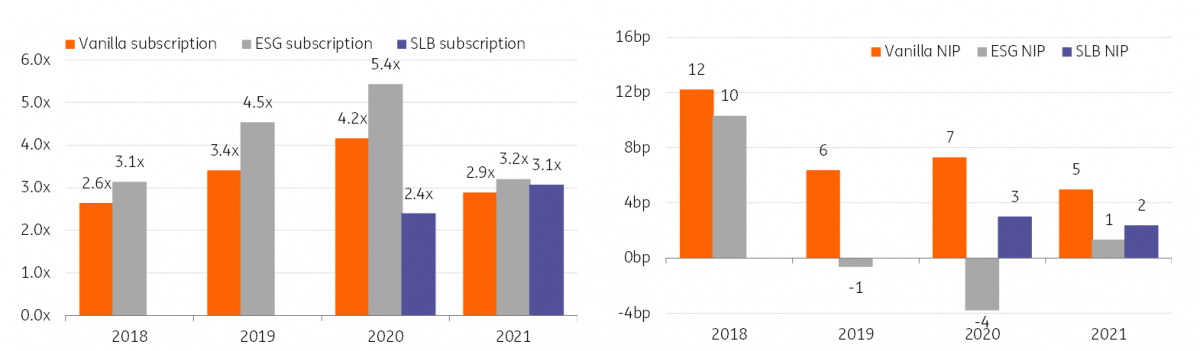

Book subscriptions are higher for ESG, but premiums are lower

We see continuous inflows into ESG funds, adding further demand for ESG products. In the last twelve months, from October 2022 to October 2023, flows into EUR IG ESG accumulated to c.13%. Additionally, during times of outflows from credit, ESG funds generally remain positive.

Inflows into ESG € IG corporate funds continue to grow

The high demand for corporate ESG bonds is reflected in bond subscription levels. In the first ten months of 2023, corporate € sustainability-linked bonds were 3.5x oversubscribed, green bonds 3.2x and plain vanilla bonds 2.9x. Looking back to the period 2018-2022, green and SLB bonds have seen higher subscription levels than plain vanilla bonds – with an exception in 2020 when SLBs’ book subscriptions came in under plain vanilla). Globally, we expect the picture in 2024 to remain in line with what we have seen in the last three years.

Despite a mixed picture across the years, the period 2018-2023F tends to show that corporate € IG vanilla bonds have paid a higher premium on the market. We believe that moderate corporate ESG supply, like the one we forecast for 2024 at €90bn, will push investors towards accepting lower premiums for their participation in new ESG issuances.

Book subscription are higher for ESG but premiums are lower

We forecast €75bn in EUR financial ESG supply in 2024

Sustainable bank bond supply on track to reach new highs in 2023

Banks remained very active in the sustainable bond market this year. By the end of October, credit institutions across the globe had issued over €70bn in EUR sustainable bonds. This is more than €10bn ahead of the sustainable supply over the same period in 2022. We expect green, social and sustainability issuance of banks to reach €80bn this year, up €8bn versus 2022. While banks will issue notable amounts of sustainable debt in 2024, slower lending growth will probably make it difficult for banks to continue to issue at the same pace as this year. We expect to see slightly less sustainable supply next year despite our forecasted modest rise in total bank supply.

| €75bn |

in ESG supply by banksIn 2024 |

Banks issued €19bn in 2023 YTD (27%) in sustainable debt via the covered bond market, €19bn (28%) in preferred senior, €30bn (43%) in bail-in senior and €2bn (3%) in T2 bonds. This confirms the dominant focus of the ESG issuance on bail-in senior this year. This has been more than a reflection of the general supply dynamics alone. Banks printed 31% of their bail-in senior supply with a sustainable use of proceeds. This compares with much lower shares of 19% in preferred senior, 11% in covered bonds and 10% in T2 bonds. The better observable funding cost advantages of sustainable issuance further down the liability structure form one of the reasons. Besides, the broader investor base for sustainable bonds has supported banks in issuing bail-in senior deals against a backdrop of this year’s sometimes volatile market conditions.

Sustainable issuance in bank bonds continues to rise

Green issuance continues to dominate, even though the pickup in social supply is probably more noteworthy. At €13bn YTD, social issuance is up €4bn versus last year YoY and on track to beat peak year 2021 (€14bn in social bonds). The YTD rise in social issuance almost matches the €5bn rise in green supply, which is in total four times as high as social issuance. The supply of bonds with proceed allocations to both green and social projects (i.e. sustainability supply) remains low at €2bn YTD.

Social issuance will continue to become more dominant

Factors driving sustainable bank bond supply in 2024

Slower lending growth (-)

Bank lending growth is stagnating against the backdrop of the rise in interest rate levels. This makes it difficult for banks to substantially grow their sustainable loan portfolios. That said, against the backdrop of the evolving ESG regulation and wider investor and societal push for companies and banks to become more sustainable, the sustainable loan books will still see better growth dynamics than the less sustainable loan portfolios.

Few sustainable bond repayments (-)

Redemption payments in the sustainable bank bond segment remain low, with only €18bn in EUR bonds maturing in 2024. This only frees up little space for banks to refinance maturing bonds against the same pool of sustainable assets. Moreover, part of the sustainable loans that fall free may not be refinanced via new sustainable bonds. Either because issuers have strengthened their loan eligibility criteria or because the loans no longer fall within the look-back periods that issuers apply for new issuance.

Only €18bn in EUR sustainable bank bonds fall due in 2024

Identification of new assets (+)

There are also boundaries to the further growth potential via the identification of new sustainable assets or via first-time issuers. Following the substantial issuance of the past years, more banks are reaching the limits of their available sustainable assets. Some banks also assign parts of their sustainable portfolios to deposit or commercial paper alternatives. These loans are then unavailable for sustainable bond market funding. Nonetheless, we continue to see banks financing new sustainable loan types including, for instance, via separately established social bond frameworks in addition to their existing green bond frameworks. This will remain supportive to sustainable issuance.

Evolution of the green and social portfolio versus supply of Germany’s largest issuer of sustainable bonds

Financing of other environmental objectives (+)

Green bank bonds continue to (re)finance mostly loans for the purpose of climate change mitigation. However, they could also more often start funding other environmental objectives, such as climate change adaptation. Think for instance of loans related to the implementation of physical and non-physical solutions to reduce physical climate risks as identified through climate risk and vulnerability assessments (CRVA).

In June 2023 the European Commission also published the Environmental Delegated Act, setting the technical screening criteria for the remaining four environmental objectives of the EU Taxonomy, ie sustainable use and protection of water and marine resources, transition to a circular economy, pollution prevention and control and protection and restoration of biodiversity and ecosystems. This may open further opportunities for the issuance of green bonds.

Sustainability-linked issuance (+)

Sustainability-linked bond supply is still more a corporates than a financials phenomenon. In 2023, one of the major Nordic banks issued its first EUR use of proceeds bond financing a portfolio of sustainability-linked loans (SLL) to companies with sufficiently ambitious climate change mitigation goals. Apart from that there was no sustainability linked issuance, not directly via sustainability linked bonds (SLB), or indirectly through use of proceeds instruments financing sustainability linked loans.

Use of proceeds SLL bonds have the advantage though that they do not have coupon step-up features linked to any sustainability KPIs at the level of the bond. These KPIs and interest rate step-up / step-down features are set at the level of the sustainability linked loans financed by the bonds. Hence, there are coupon characteristics at the levels of the bond that could be seen as an incentive for early redemption. This has made it difficult to issue senior or subordinated bonds in SLB format eligible for a bank’s minimum requirement for own funds and eligible liabilities (MREL).

We believe that sustainability linked issuance could develop more in the bank bond segment. Particularly against the backdrop of the Corporate Sustainability Reporting Directive (CSRD) and Corporate Sustainability Due Diligence Directive (CSDD) requiring (non-)financial companies to disclose their transition plans.

What to expect from the European Green Bond Standard

On 23 October, the European Council adopted the European Green Bond legislation, eight months after the EU reached a political agreement on the standard in February. The regulation will be signed and published in the EU’s Official Journal and will enter into force 20 days after publication in the Official Journal. The European green bond regulation should then apply twelve months after entry into force, so likely from November/December 2024 onwards. This means that towards the end of next year, issuers can officially start marketing bonds as European Green Bonds.

The European Green Bond Standard – the requirements in a nutshell

The proceeds of bonds marketed as European Green Bond should be allocated before the maturity of the bond conform the requirements from the EU Taxonomy.

Issuers may apply a portfolio approach. They can allocate the proceeds of multiple green bonds to a portfolio of taxonomy-aligned assets. When the bond proceeds are allocated to financial assets such as loans, the loans should in principle not be created later than five years after issuance of the European green bond, unless the portfolio approach is used.

The European green bond regulation provides for a so-called flexibility pocket. Up to 15% of the proceeds can be allocated to economic activities that comply with the EU taxonomy apart from the technical screening criteria, for instance because these criteria have not entered into force yet. The activities funded should still contribute substantially to one of the taxonomy’s environmental objectives. The relevant generic ‘do no significant harm’ provisions should also be met.

Importantly, if the technical screening criteria are amended before the maturity of the European green bond, the bond will keep its European green bond status if the proceeds were allocated based upon the old technical screening criteria. Only the unallocated proceeds, and proceeds covered by a CapEx plan assuring their forthcoming taxonomy alignment, will have to be allocated conform the new technical screening criteria within seven years. When a portfolio approach is applied, the assets not meeting the amended technical screening criteria can stay part of the green portfolio for seven years at most.

The European green bond regulation also subjects issuers of European green bonds to stricter transparency requirements by requiring the publication of a (pre-issuance) green bond factsheet and a (post-issuance) allocation and impact reports. To facilitate comparability, public disclosure templates will be established for other environmentally sustainable bonds and sustainability linked bonds, including on the taxonomy alignment. To this purpose the European Commission will establish guidelines for voluntary pre-issuance disclosure and a delegated act for periodic disclosures, in line with the European green bond factsheet and allocation report.

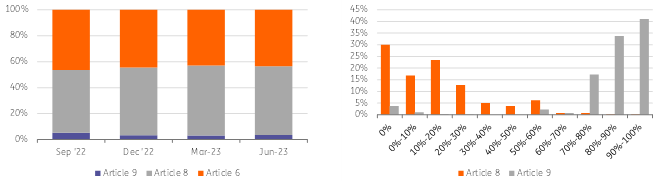

Bonds marketed as European green bond do count as 100% taxonomy aligned for the Taxonomy KPI disclosures of asset managers and banks. The bonds should also be eligible for inclusion in Article 9 funds (sustainable investments). Investors may therefore prefer bonds with a European green bond designation. That said, other green bonds also contribute to the Taxonomy KPIs of investors to the extent that the bond proceeds are used to finance Taxonomyalligned activites. Moreover, against the backdrop of the ESMA’s clarification in 2022 that SFDR Article 9 funds should be comprised for 100% of sustainable investments, most funds remain classified as Article 8 (promoting environmental or social characteristics). Data of Morningstar Direct confirm that most Article 8 funds do not require more than 30% of the investments to be sustainable. This means green bonds that are not 100% taxonomy compliant will still be met with a notable investor appetite.

Most of the assets under management are Article 8 with only few of the Article 8 funds require >50% sustainable investments

Against this backdrop, it remains yet to be seen if the issuance of European green bonds will pick up significantly per the end of next year. Particularly as some issuers may still feel reluctant to market their green bonds as 100% taxonomy compliant. Ensuring 100% taxonomy compliance means banks not only have to be sure that loans in their green portfolios meet the EU taxonomy criteria for substantial contribution, but also that the applicable do no significant harm criteria and minimum safeguards are met.

Bonds financing energy efficient residential real estate assets may still be well suited to be marketed as European green bonds. These bonds would only have to meet the do no significant harm provisions for climate change adaptation as per the relevant climate change mitigation criteria for acquisition and ownership of buildings. To our understanding this also applies to loans that finance the acquisition of houses built after December 2020. These provisions solely come down to the performance of a climate risk and vulnerability assessment (CRVA) to identify physical climate risks such as floods, and to the development of an adaptation solutions plan to reduce these risks if material.

The applicable do no significant harm criteria per real estate activity

In the final report on the minimum safeguards of October 2022 the Platform on Sustainable Finance also clarified that households are not considered to be covered by the minimum safeguards under the EU taxonomy. Hence the minimum safeguard provisions would not apply to mortgages granted to households for house purchases.

In summary

We expect banks to issue €75bn in sustainable EUR debt in 2024, €5bn less than our full-year estimate for 2023. We believe slower lending growth will make it difficult for banks to continue to issue sustainable bonds at the same pace as this year, particularly with more and more issuers reaching the boundaries of their issuance capacity against the existing portfolios of sustainable assets.

That said, sustainable supply will continue to be lively in our view, as banks will remain resourceful in the identification of new assets suitable for ESG issuance. Against this backdrop, we expect a modest further rise in social issuance (€17bn), even though green supply is set to decline (€53bn). Meanwhile, banks will continue to prepare for the first issuance under European green bond regulation. However, such issuance will not take place before the end of 2024 however.

We forecast €50bn in high yield corporate supply in 2024

We expect the European high yield primary corporate euro-denominated supply to pick up in 2024 relative to our expectations for the current year. To provide a proper context, the Euro high yield (EHY) new issuance was severely constrained during 2022 due to a combination of low urgent refinancing needs, a sharp rise in interest rates and a geopolitical shock of Russia’s full-scale invasion of Ukraine. We believe that the transition mode to the new “higher for longer” paradigm partially continued in 2023, with periods of very low or complete halt of primary activity still present during this year. However, on balance, we feel that the period of adjustment is nearing its end while the new realities, including the need to fund or pre-fund upcoming maturities are asserting themselves.

With this in mind, we expect that gross EHY euro-denominated corporate supply will step up to €50bn in 2024 from our current expectation of €36bn for FY23. In our view, this will stem primarily from the need to address and pre-fund the upcoming debt maturities falling due in 2024 and 2025. We estimate that the proverbial maturity wall in the European high yield bond space will not yet transpire next year, while redemptions will ratchet up during 2025 and, in particular, in 2026. Therefore, we expect pre-funding or rolling over of the existing debt to represent €40bn in 2024, with a modest balance of €10bn representing additional funding needs.

We feel that there is a potential upside to our FY24 gross EHY corporate supply forecast but to add a word of caution, this also assumes a fairly benign market environment, with no major dislocations or only relatively contained episodes of heightened risk aversion. In the end, with the benchmark rates not retracing themselves yet any further elevated risk premia will act as a disincentive or be prohibitive for some of the issuers while investors may prefer to stay on the sidelines during such periods. On balance, our supply forecast assumes that the EHY market should have a constructive tone for significant enough stretches of next year to allow the refinancing or pre-funding of the growing redemption requirements. We will address our EHY return expectation for FY24 in our upcoming Credit Outlook publication.

European High Yield Supply

We forecast €12bn in EUR Real Estate supply in 2024

Increase in supply but from very low levels. Still, expect negative net supply

2023 supply is the lowest since the Great Financial Crisis era at around €6.7bn year to date, as of October 2023. This is a result of plummeting real estate transaction volumes, yield expansion and real estate valuations continuing to decline, which has led to high levels of market uncertainty and high spread levels, effectively ‘shutting’ bond market access for many real estate companies since late 2022.

We expect another year of low new issuance in the real estate market in EUR for 2024, although we are forecasting new issuance to nearly double year-on-year to €12bn. We think that interest rates and swap rate stabilisation could lead to more supply from higher-quality issuers. We also expect a higher transaction volume in 2024, which is also likely to support supply. A further stabilisation in real estate valuations and improving sentiment in the latter part of 2024 could also help to ‘re-open ‘ the real estate bond market.

Net supply is still expected to remain strongly negative at -€8bn, only the second year of negative supply in recent history following -€13bn net supply we have seen in 2023 so far.

Redemptions in 2024 are similar to 2023 at €21bn, although these start to increase quite strongly thereafter (2025 = €25bn; 2026 = €28bn; 2027 = €27bn). This may lead to a higher level of early pre-funding in the second half of 2024, particularly if other types of funding (bank secured debt, equity) become more difficult to access and deleveraging through asset disposals remains constrained.

Supply to pick up, but from very low levels

Download

Download article

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more