Commodities: So much for OPEC+ cuts

The oil market has given back all of its gains made following the latest OPEC+ supply cut announcement. Instead, it's the macro story which has dictated price action. While there may be a bit more downside in the near term, the outlook for the second half of the year remains constructive on the back of tighter fundamentals

Oil fundamentals still constructive

The sell-off in the market has been unrelenting over recent weeks, with negative sentiment rising following concerns over the macro environment and what it could eventually mean for oil demand. In addition, weaker refinery margins have also raised doubts over the strength of oil demand. Part of the weakness in margins is also driven by supply dynamics, with Russian refined product flows holding up well, whilst in Asia, Chinese refined exports remain strong.

Global oil demand is expected to grow by around 1.9MMbbls/d in 2023, compared to our previous forecast of 2MMbbls/d. This revision is largely driven by the US, where our macro team is expecting the economy to contract by a fairly sizeable amount over the latter part of the year. Approximately 90% of global demand growth will be driven by non-OECD countries.

On the supply side, the oil market has been dealing with continued disruptions to oil flows from Northern Iraq via Ceyhan in Turkey. This is after a court ruled in favour of the Iraqi government in a dispute over Kurdish flows via Turkey. The stoppage is holding around 450Mbbls/d from the market, which has been the case since late March. Iraq is still in talks with Turkey, but it is not yet clear when flows will resume.

As for Russia, seaborne export flows continue to hold up well, with volumes still at pre-war levels. The impact of import bans and price caps has therefore had a much more limited impact on flows than initially thought.

Expectations for 2023

While the oil market has been well supplied so far in 2023, it is expected to tighten significantly over the second half of the year. Demand growth largely from non-OECD countries combined with OPEC+ supply cuts should see the market drawing down inventories over the latter part of the year. While we will see growth in US supply, it will be much more modest than growth in previous years and not enough to prevent a large deficit later this year. The action that we have seen from OPEC+ in recent months also suggests that the group is fully aware of limited supply growth from non-OPEC+ members. The group is confident that they can cut output without the risk of losing a large amount of market share. If we were to see further downward pressure in oil prices over the coming months, OPEC+ could be forced to act by reducing supply even further.

However, we expect oil prices to move higher from current levels due to the deficit environment over the second half of the year – although slightly weaker demand expectations and sticky Russian supply mean that this deficit is not as large as initially expected. As a result, we have revised lower our price forecast for Brent from US$101/bbl to US$96/bbl over the second half of 2023

2023 global oil demand growth driven by non-OECD (MMbbls/d)

Injection season well underway for the European gas market

The European gas market has been a lot more subdued relative to the oil market over the last month. However, macro concerns along with weaker demand over the shoulder months have driven natural gas prices lower. TTF is trading below EUR40/MWh and has recently traded down to levels last seen in July 2021.

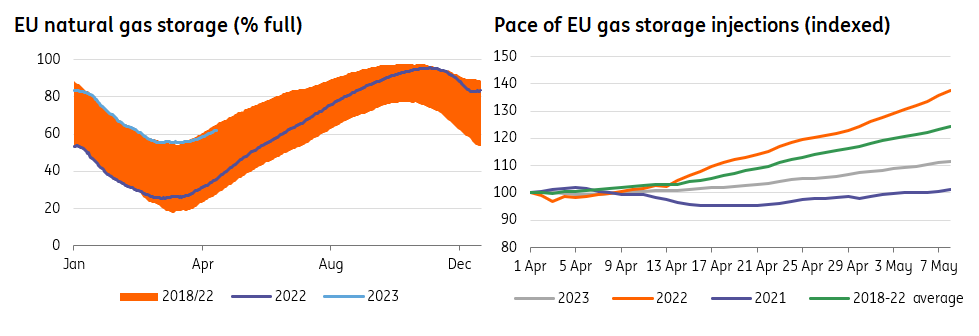

The end of winter has meant that Europe has started its injection season. Storage is currently around 62% full, well above the 36% seen at the same stage last year, and also higher than the five-year average of 42%. This puts the region in a good position to hit its target of having storage 90% full by 1st November. It also means that we do not need to see European buyers scramble like they did last year to ensure enough supply. Storage data already shows that net injections since the end of winter have been at a much slower pace than last year.

There also seems to be limited buying interest for LNG from Asia, which only adds to the downward pressure on global gas prices. Chinese LNG imports over the first quarter were down 4.9% year-on-year, already falling short of expectations. Spot Asian LNG continues to trade at a small discount to TTF, a trend that is also seen further along the forward curve.

Looking ahead: Risks for Europe

As for European gas, it appears as though we are still yet to see a strong recovery in industrial demand. In April, German industrial gas demand was 12.1% below the 2018-21 average, while total consumption was down just 5.9% from the average due to stronger household demand. We'll need to keep an eye on how demand responds in the coming months for more clarity on just how much of the recent drop is likely permanent. Our balance suggests that demand only needs to be around 10% below the five-year average rather than the European Commission’s 15% voluntary cut, which has been extended until the end of next winter.

In the absence of any supply shocks, it's difficult to see significant upside in the near term with decent storage levels. We believe that Europe should enter the 2023/24 winter in a comfortable situation. However, assuming normal conditions, the EU will draw down inventories at a quicker pace over the next winter. We could finish the 2023/24 heating season with storage closer to the five-year average, while stronger draws (relative to the 2022/23 winter) should push prices higher. We forecast TTF to move up towards the EUR60-65/MWh range over the 2023/24 winter. This remains unchanged from last month.

Upside risks to this view would be a colder winter than usual, stronger Asian LNG demand over the second half of the year, and Russia cutting off remaining pipeline flows to Europe. A combination of these three events could leave Europe under extremely tight circumstances by the end of the next winter.

Pace of EU gas injections slower but storage still very comfortable

Download

Download article

12 May 2023

ING Monthly: We’re in a polycrisis – and this is what it means This bundle contains 16 articlesThis publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more