Soybean area likely to grow next year

The increase in buying we have seen from China, along with the strength in soybean prices means that we are likely to see soybean area continue to grow in 2021/22, while corn acres are likely to be slightly down to flat

US to boost soybean area

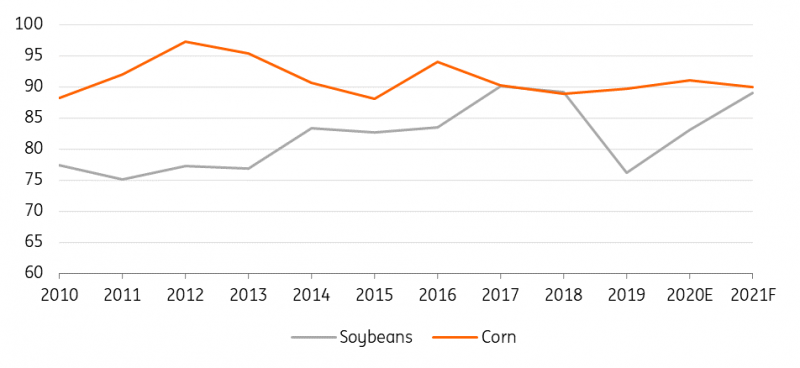

Over recent years, the US has seen fairly big shifts in soybean planting, with the trade war putting pressure on the soybean market and farmers shifting acres to corn.

However, with China back in the market for US agricultural products, along with better weather in the planting season this year, soybean area in 2020/21 has grown by around 9.2% year-on-year to 83.1m acres, but this is still significantly below pre-trade war levels of 90.2m acres that we saw in the 2017/18 season.

Meanwhile, corn planted area in the US has remained more stable, despite a wet planting season delaying plantings in 2019/20. In 2020/21, planted area for corn is estimated to be 91m acres, which is slightly up from the pre-trade war level of 90.2m acres in 2017/18. We have seen some shifting away from soybeans to corn over this period, with the soybean/corn ratio falling to a five-year low.

We are likely to see a further increase in soybean plantings over 2021

That said, the recent rally in soybean prices has seen the soybean/corn ratio strengthening to around 2.8 in the prompt contracts, while if we look at the forward curves, and in particular towards the end of 2021, the ratio is a little over 2.5. Historically, a price ratio of around 2.5 acts as the tipping point for soybean/corn switching, with farmers tending to switch to soybean if the price ratio is above this level. This suggests that we are likely to see a further increase in soybean plantings over 2021, with area likely to increase to somewhere in the region of 89-90m acres for the 2021/22 marketing year. The USDA in its long-term planting projections estimates soybean acreage to grow to 89m acres in 2021/22, whilst corn plantings are estimated to fall slightly to 90m acres.

If we assume yields are aligned with the five-year average for 2021/22, we could see a US soybean harvest which amounts to a little over 4.4b bushels, up from an estimated 4.17b bushels this season and reaching levels last seen during the 2018/19 season. For corn, assuming a yield similar to the five-year average, we would likely see the US corn crop over next season decline YoY from 14.5b bushels to somewhere a little below 14.3b bushels.

US planted area- soybean vs corn (m acres)

Weather concerns for South America

Looking south, Brazil’s agricultural agency Conab expects soybean area in the country to increase 3.5% YoY to 38.2m ha in 2020/21, despite a late start to plantings, as stronger prices encourage farmers to plant more.

Soybean prices in Brazil have been well supported by strong Chinese demand, while a weaker Brazilian real has meant that farmers have seen stronger margins in BRL terms

Soybean prices in Brazil have been well supported by strong Chinese demand, while a weaker Brazilian real has meant that farmers have seen stronger margins in BRL terms. This increased area means that Brazil is set to harvest a record crop of a little under 135mt in 2020/21, up more than 8% YoY. However given the dry weather that we have seen in the region over recent months, which slowed plantings, there are concerns over what this could mean for productivity, and so there is certainly downside risk to Conab's record production estimate. Corn acreage in Brazil is expected to drop marginally from 18.5m ha in 2019/20 to 18.4m ha in 2020/21 although expectations of an improvement in yields are forecast to push total corn output in the country to a record 104.9mt, up 2.3% YoY.

In Argentina, dry weather between September and October delayed corn plantings, with farmers having the option for late-season corn (to be planted in December) or a switch to soybean, which is usually planted in October-December. The Buenos Aires Grains Exchange expects that total soybean area this year will increase marginally from 17.1m ha last season to 17.2m ha in 2020/21, however, given expectations of lower yields, total soybean output from the country is expected to fall from 49mt to 46.5mt.

Corn is expected to see area fall by 3% YoY and coupled with expectations of poorer yields, this means that the corn crop is forecast to fall almost 9% YoY to 47mt.

Download

Download article

8 December 2020

ING’s Commodities Outlook 2021 This bundle contains 11 articlesThis publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more